Understanding Systematic Investment Plans (SIP)

A comprehensive guide for Indian investors to understand how SIPs work, their benefits, and how to start building long-term wealth.

- NV Trends

- 6 min read

Building wealth does not always require a large sum of money upfront. For many middle-class Indian families, the dream of buying a house, funding a child’s higher education, or planning a peaceful retirement can feel overwhelming. However, there is a simple financial tool that has transformed the way India invests: the Systematic Investment Plan, commonly known as SIP.

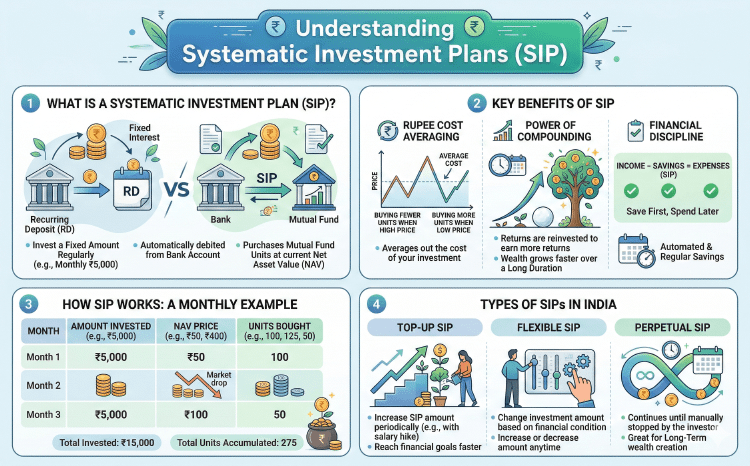

What is a Systematic Investment Plan (SIP)?

A Systematic Investment Plan is not an investment product itself, but rather a method of investing in mutual funds. Think of it like a Recurring Deposit (RD) that you might have with a bank, but instead of the money going into a savings account, it goes into a mutual fund scheme of your choice.

With an SIP, you commit to investing a fixed amount of money at regular intervals—usually monthly. This money is automatically debited from your bank account and used to purchase units of a mutual fund at the prevailing Net Asset Value (NAV).

Key Takeaways

- SIPs allow you to start small, with as little as ₹500 per month.

- They instill financial discipline by making saving a regular habit.

- Rupee Cost Averaging helps you manage market volatility without timing the market.

- The power of compounding works best when you stay invested for a long duration.

- It is a flexible tool where you can stop, skip, or increase your investment at any time.

Why SIP is Ideal for the Indian Investor

In India, market volatility is a common concern. Many people avoid the stock market because they fear losing their hard-earned money during a market crash. SIPs are designed to address this exact fear.

1. Rupee Cost Averaging

This is perhaps the biggest advantage of an SIP. Since you invest a fixed amount every month, you end up buying more units when the market is low and fewer units when the market is high. Over time, this averages out the cost of your investment. You don’t have to worry about whether the Sensex is at 70,000 or 60,000; the system works for you regardless of market cycles.

2. The Power of Compounding

In the world of finance, time is more important than money. When you invest through an SIP, the returns you earn are reinvested, and you start earning returns on those returns. For an Indian youngster starting their first job at age 22, even a small SIP of ₹2,000 can grow into a massive corpus by the time they reach age 50, thanks to the compounding effect over nearly three decades.

3. Financial Discipline

Most Indians follow the traditional formula: Income - Expenses = Savings. Unfortunately, with rising lifestyle costs, there is often nothing left to save. SIP flips this formula to: Income - Savings (SIP) = Expenses. By automating your investment at the start of the month, you ensure that your future is prioritized before you spend on current wants.

How Does an SIP Work in Practice?

When you start an SIP, you choose a date (e.g., the 5th of every month). On this date, ₹5,000 (for example) is moved from your bank to the mutual fund house.

If the NAV of the fund is ₹50, you get 100 units. If next month the market falls and the NAV becomes ₹40, your ₹5,000 buys you 125 units. If the following month the market rises and the NAV is ₹100, you get 50 units.

Over these three months, you have invested ₹15,000 and accumulated 275 units. This process continues, building your “pot of gold” one month at a time.

Types of SIPs Available in India

The Indian mutual fund industry offers various types of SIPs to suit different needs:

Top-up SIP

This allows you to increase your SIP amount periodically. For instance, if you get a yearly salary hike of 10%, you can increase your SIP by 10% as well. This helps you reach your financial goals much faster.

Flexible SIP

In a flexible SIP, you can change the investment amount based on your financial condition. If you have an emergency one month, you can reduce the amount, or if you get a bonus, you can increase it.

Perpetual SIP

When filling out an SIP form, if you don’t provide an end date, it becomes a perpetual SIP. This is great for long-term wealth creation as it continues until you manually give an instruction to stop it.

Common Myths About SIPs

Myth 1: SIPs are only for small investors

While SIPs are great for small investors, many wealthy individuals and High Net-worth Individuals (HNIs) also use SIPs to manage their large portfolios and ensure they don’t enter the market at a single peak price.

Myth 2: You cannot lose money in an SIP

SIPs reduce risk, but they do not eliminate it. Since the money is invested in the market, the value of your portfolio can go down if the market crashes. However, for long-term investors (5-10 years+), the probability of negative returns in equity SIPs has historically been very low in India.

Myth 3: I should stop my SIP when the market is down

This is the most common mistake Indian investors make. When the market is down, your SIP is buying units at a “discount.” Stopping your SIP during a crash is like refusing to buy gold when the price drops. To benefit from Rupee Cost Averaging, you must keep the SIP running during market lows.

How to Start Your SIP Journey

Starting an SIP in India today is easier than ever. Here is a step-by-step guide:

- Complete Your KYC: You need a PAN card, Aadhaar card, and a bank account. Most platforms allow you to complete your KYC digitally.

- Define Your Goal: Are you saving for a wedding, a car, or retirement? Knowing your goal helps you choose the right type of fund (Equity, Debt, or Hybrid).

- Choose a Mutual Fund: Research funds based on their past performance, the reputation of the Fund House (AMC), and the fund manager’s track record.

- Select the Date and Amount: Choose a date shortly after your salary is credited. Start with an amount you are comfortable with.

- Automate: Set up an E-Mandate so the money is deducted automatically. This removes the “laziness factor” from investing.

Conclusion

The Systematic Investment Plan is a testament to the fact that “slow and steady wins the race.” For the Indian investor, it provides a path to participate in the country’s economic growth without needing to be an expert in stock market technicals.

By starting an SIP today, you are not just saving money; you are buying freedom for your future self. Whether the markets go up or down tomorrow, your disciplined approach will ensure that you are building a solid foundation for your family’s dreams. Remember, the best time to start an SIP was yesterday; the second-best time is today.