Top 5 Mutual Funds for Conservative Investors

Discover the best low-risk mutual fund options in India for conservative investors seeking capital preservation and steady growth in 2026.

- NV Trends

- 5 min read

For many Indian investors, the safety of their hard-earned money is the top priority. While the stock market often makes headlines with stories of massive gains, the reality is that not everyone has the stomach for high volatility. If you are someone who prefers a peaceful night’s sleep over the adrenaline rush of mid-cap stocks, you fall into the category of a conservative investor.

In the Indian financial landscape of 2026, conservative investing doesn’t mean you have to settle for meager returns. By choosing the right mutual funds, you can protect your capital while earning returns that comfortably beat inflation and traditional savings accounts.

Who is a Conservative Investor?

Before diving into the specific fund recommendations, it is important to understand what makes an investor “conservative.” A conservative investor typically prioritizes capital preservation over high growth. You might be a retiree looking for regular income, a parent saving for a child’s education in the near term, or simply someone who is risk-averse by nature.

In India, conservative investors have traditionally relied on Fixed Deposits (FDs) and Public Provident Fund (PPF). However, with changing interest rate cycles, mutual funds offer a more tax-efficient and flexible alternative.

The Strategy for Conservative Portfolios

A conservative portfolio usually leans heavily toward debt instruments with a small exposure to equity to provide a “kicker” for returns. The goal is to minimize the “downside”—the amount you could lose during a market crash—while participating slightly in the “upside” when the economy grows.

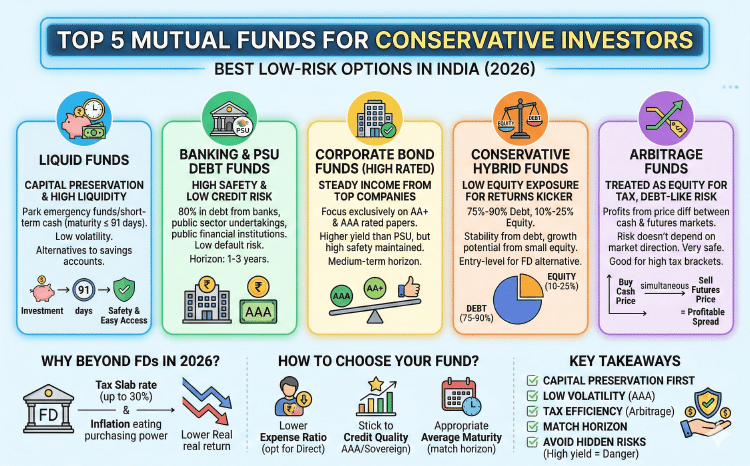

1. Liquid Funds: The Cash Alternative

Liquid funds are the bedrock of conservative investing. These funds invest in very short-term debt instruments like treasury bills and commercial papers that mature within 91 days.

They are ideal for parking your emergency fund or money you might need in a few months. In 2026, liquid funds continue to be a favorite because they offer high liquidity and carry negligible interest rate risk. They generally provide better returns than a standard savings bank account while keeping your money accessible.

2. Banking and PSU Debt Funds

For those who want safety similar to a bank FD but with potentially better tax efficiency, Banking and PSU funds are excellent. These funds invest at least 80% of their assets in debt instruments issued by banks, public sector undertakings (PSUs), and public financial institutions.

Because these institutions are often backed by the government or are “too big to fail,” the credit risk (the risk of default) is extremely low. These are suitable for an investment horizon of 1 to 3 years.

3. Corporate Bond Funds (High Rated)

Corporate bond funds invest in debt papers issued by private companies. For a conservative investor, the focus must remain on funds that invest exclusively in ‘AA+’ or ‘AAA’ rated papers. These ratings indicate the highest level of safety.

While they carry slightly more risk than PSU funds, they offer a higher yield. They are a great way to earn steady interest income over a medium-term horizon.

4. Conservative Hybrid Funds

If you are willing to take a tiny bit of risk for better-than-debt returns, Conservative Hybrid Funds are the way to go. These funds invest 75% to 90% of their total assets in debt and the remaining 10% to 25% in equity (stocks).

The debt portion provides stability and regular income, while the small equity portion helps the fund grow faster than a pure debt fund. This is a perfect “entry-level” fund for someone moving from FDs to mutual funds.

5. Arbitrage Funds

Arbitrage funds are a unique category that is technically treated as an equity fund for taxation but behaves like a debt fund in terms of risk. They profit from the price difference between the cash market and the futures market.

Since the fund manager buys in one market and sells in another simultaneously, the market direction doesn’t matter. They are very safe and are particularly attractive for investors in high tax brackets because of their favorable tax treatment.

Why Move Beyond Fixed Deposits in 2026?

While FDs are simple, they have two main drawbacks in the current Indian economy:

- Taxation: FD interest is added to your income and taxed at your slab rate. If you are in the 30% bracket, your real return drops significantly.

- Inflation: Often, the post-tax return of an FD is lower than the inflation rate, meaning your purchasing power is actually shrinking.

Mutual funds, especially through systematic withdrawal plans (SWP), can provide a more efficient way to manage your wealth.

How to Choose the Right Fund for You

When selecting a fund from the categories mentioned above, keep these three factors in mind:

Expense Ratio

Since conservative funds have lower return expectations than aggressive equity funds, a high expense ratio can eat up a large chunk of your profits. Always look for funds with lower expense ratios, or better yet, opt for ‘Direct’ plans.

Credit Quality

Never chase high yields in debt funds. If a debt fund is offering significantly higher returns than its peers, it might be taking on “credit risk” by lending to lower-rated companies. For a conservative investor, safety is more important than that extra 1% return.

Average Maturity

This tells you how sensitive the fund is to changes in interest rates. Funds with shorter average maturity are less volatile when interest rates fluctuate.

Key Takeaways

- Safety First: Conservative investors should prioritize funds with high credit ratings (AAA) and low volatility.

- Diversify: Even within a low-risk strategy, don’t put all your money in one fund. Spread it across Liquid, PSU Debt, and Hybrid categories.

- Tax Efficiency: Use Arbitrage funds or Debt funds held for the long term to manage your tax liability better than FDs.

- Investment Horizon: Match your fund choice to your needs. Use Liquid funds for months, and Hybrid funds for years.

- Avoid Greed: In the debt market, unusually high returns usually signal hidden risks. Stick to the top-rated, well-established fund houses.

Conclusion

Conservative investing is not about being afraid; it is about being smart with your capital. By utilizing the top 5 mutual fund categories discussed—Liquid, Banking/PSU, Corporate Bond, Conservative Hybrid, and Arbitrage funds—you can build a robust portfolio that stands the test of time.

The Indian market in 2026 offers plenty of opportunities for steady growth without requiring you to take unnecessary risks. Start small, stay consistent, and let the power of compounding work for you in a safe and secure environment.