Top 5 Debt Funds for Safe Returns

Looking for stable returns with lower risk? Explore the top 5 debt mutual funds in India for 2026 to protect your capital and earn steady income.

- NV Trends

- 6 min read

In the ever-changing landscape of the Indian financial market, investors often find themselves torn between the desire for high growth and the need for capital preservation. While equity markets grab the headlines with their spectacular rallies, the foundation of a sound financial plan often lies in the stability provided by debt instruments. For the conservative Indian investor, debt mutual funds offer a compelling alternative to traditional fixed deposits, providing better liquidity and the potential for superior post-tax returns.

As we move through 2026, understanding where to park your surplus cash for “safe” returns is more crucial than ever. Debt funds invest in fixed-income securities like government bonds, corporate debentures, and money market instruments. They are designed to provide steady interest income and modest capital appreciation.

In this comprehensive guide, we will dive deep into the world of debt funds and identify the top five categories that are currently offering the best balance of safety and returns for Indian investors.

Why Debt Funds are Essential for Your Portfolio

Many investors view debt funds simply as a place to keep money for a short duration. However, their role is much more significant. Debt funds act as a shock absorber during equity market volatility. When the stock market dips, your debt allocation remains relatively stable, ensuring that your overall portfolio value doesn’t plummet.

Furthermore, debt funds offer much higher flexibility than Bank Fixed Deposits (FDs). While FDs often come with premature withdrawal penalties, most debt funds allow you to exit within a few days or months with minimal or no exit load.

Key Takeaways

- Debt funds provide stability and capital preservation in a volatile market.

- They are more liquid and often more tax-efficient than traditional savings schemes.

- Liquid and Overnight funds are ideal for very short-term surpluses.

- Corporate Bond funds offer a higher yield by investing in high-rated company debt.

- Banking and PSU funds provide high safety due to their exposure to government-backed entities.

- Always check the credit quality and duration of a fund before investing.

The Top 5 Debt Funds for Safe Returns in 2026

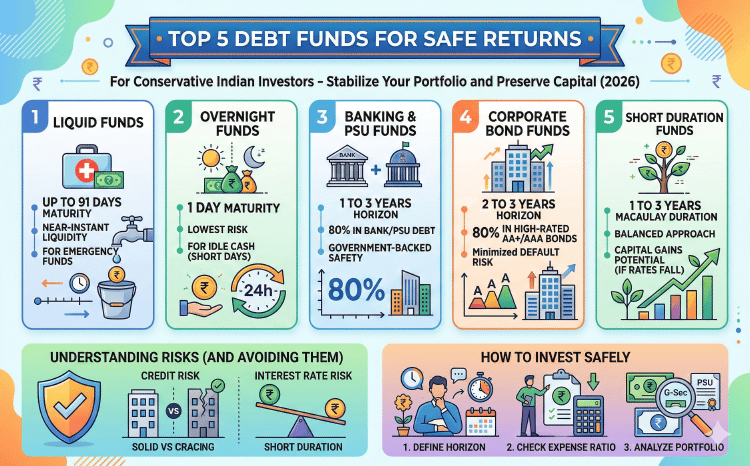

1. Liquid Funds

Liquid funds are the gold standard for safety and liquidity. These funds invest in highly secure debt instruments with a maturity of up to 91 days. They are the perfect place to park your emergency fund or money that you might need within the next few weeks or months.

The primary advantage of liquid funds is the near-instant access to your money. Many fund houses offer “instant redemption” facilities where you can get up to ₹50,000 back in your bank account within minutes. In 2026, with interest rates stabilizing, liquid funds continue to offer returns that are consistently better than a standard savings account.

2. Overnight Funds

If your primary concern is absolute safety and you have a very short investment horizon (even just one day), Overnight funds are the answer. These funds invest in securities that mature in exactly one day.

Because the maturity is so short, these funds have the lowest interest rate risk. While the returns might be slightly lower than liquid funds, the risk of capital loss is almost zero. This makes them an excellent choice for businesses or individuals who have large sums of money sitting idle for just a few days.

3. Banking and PSU Funds

For investors looking for a “safe” harbor for a period of 1 to 3 years, Banking and PSU funds are highly recommended. These funds are mandated to invest at least 80% of their assets in debt instruments issued by banks, Public Sector Undertakings (PSUs), and Public Financial Institutions.

In the Indian context, PSUs and large banks have a very high credit rating because they are often backed by the government. This gives investors peace of mind regarding the safety of their principal. These funds typically provide higher returns than liquid funds while maintaining a high safety profile.

4. Corporate Bond Funds

Corporate bond funds invest at least 80% of their portfolio in the highest-rated corporate bonds (typically AA+ and above). These funds are suitable for investors with a medium-term horizon of 2 to 3 years who are willing to take a slightly higher risk than PSU funds in exchange for better yields.

The key to success in this category is the fund manager’s ability to pick high-quality companies. By focusing on “AAA” rated papers, these funds ensure that the risk of default is kept to a minimum while capturing the higher interest rates offered by private sector giants.

5. Short Duration Funds

Short duration funds invest in debt and money market instruments such that the portfolio’s Macaulay duration is between 1 to 3 years. They are slightly more sensitive to interest rate changes than liquid funds but offer the potential for capital gains if interest rates in the economy fall.

These funds are ideal for goals that are 2-3 years away, such as a down payment for a house or a planned wedding. They offer a balanced approach to debt investing, focusing on both interest income and minor price appreciation of the underlying bonds.

Understanding the Risks in Debt Funds

While we label these funds as “safe,” it is important to understand that no investment is entirely risk-free. There are two main types of risks associated with debt funds:

Credit Risk

This is the risk that the company or entity that borrowed the money fails to pay back the interest or the principal. To stay safe, investors should look for funds with high exposure to ‘AAA’ or ‘Sovereign’ rated instruments. Avoid funds that chase high returns by investing in low-rated (junk) bonds.

Interest Rate Risk

Bond prices have an inverse relationship with interest rates. When interest rates in the economy go up, bond prices fall, and vice versa. Funds with longer durations are more sensitive to these changes. By sticking to the categories mentioned above—which mostly have short to medium durations—you can significantly reduce this risk.

How to Invest Safely in 2026

Step 1: Define Your Time Horizon

Match your investment with the fund’s duration. If you need money in 3 months, don’t invest in a Short Duration fund; stick to a Liquid fund.

Step 2: Check the Expense Ratio

Since debt fund returns are generally in the range of 6% to 8%, a high expense ratio can eat up a significant portion of your gains. Always compare the expense ratios and consider investing in “Direct” plans to maximize your returns.

Step 3: Analyze the Portfolio

Before hitting the ‘invest’ button, look at the fund’s factsheet. See where the money is going. If you see a lot of unknown private companies, the fund might be taking higher credit risks. A safe fund will have a portfolio filled with Government Securities (G-Secs), PSU bonds, and top-tier bank certificates.

Conclusion

Debt mutual funds are an indispensable tool for every Indian investor. Whether you are looking to build a safety net, save for a short-term goal, or simply diversify your portfolio, the categories mentioned above provide a robust starting point. By prioritizing Banking & PSU funds, Corporate Bond funds, and Liquid funds, you can achieve a level of safety that rivals traditional savings while enjoying the modern benefits of mutual fund investing.

Always remember that safety in debt investing comes from discipline and due diligence. Stay informed, monitor your portfolio periodically, and let your money grow steadily and securely.