Tax Saving Strategies Through Mutual Funds

Discover how to save tax and build wealth simultaneously using Equity Linked Savings Schemes (ELSS) and other mutual fund strategies in India.

- NV Trends

- 5 min read

As the end of the financial year approaches, most Indian taxpayers begin a frantic search for the best way to save on their income tax. While traditional options like Public Provident Fund (PPF) and Life Insurance have been favorites for decades, modern Indian investors are increasingly turning toward mutual funds. Specifically, Equity Linked Savings Schemes (ELSS) have emerged as a powerful tool to not only reduce tax liability but also to generate significant wealth over the long term.

In this guide, we will explore various tax-saving strategies through mutual funds, focusing on how you can optimize your portfolio to keep more of your hard-earned money while participating in India’s economic growth.

Understanding Section 80C and ELSS

The primary gateway for tax saving in India is Section 80C of the Income Tax Act. It allows individuals to claim a deduction of up to ₹1.5 lakh from their total taxable income. Among the various instruments eligible under this section—such as National Savings Certificate (NSC) and Fixed Deposits—ELSS stands out for its unique benefits.

What is ELSS?

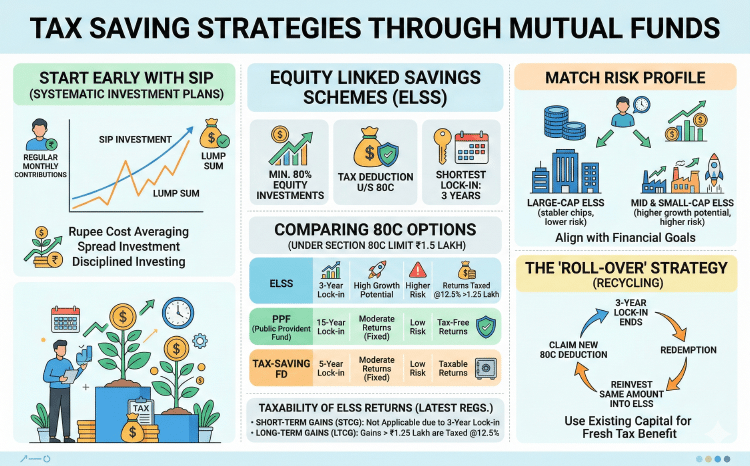

An Equity Linked Savings Scheme (ELSS) is a type of mutual fund that invests a minimum of 80% of its total assets in equity and equity-related instruments. It is the only mutual fund category that offers tax benefits under Section 80C.

Why Choose ELSS over Traditional Options?

Compared to PPF (15-year lock-in) or Tax-Saving FDs (5-year lock-in), ELSS has the shortest lock-in period of just three years. Furthermore, because it is equity-oriented, it offers the potential for much higher returns, helping you beat inflation more effectively than fixed-income instruments.

Key Takeaways

- ELSS provides tax deductions up to ₹1.5 lakh under Section 80C.

- It has the shortest lock-in period (3 years) among all 80C options.

- Investing through a Systematic Investment Plan (SIP) helps average out costs.

- Diversification within ELSS funds reduces risk while maximizing growth.

- Long-term capital gains (LTCG) tax rules apply to withdrawals.

Effective Tax-Saving Strategies

1. Start Early with Systematic Investment Plans (SIP)

One of the biggest mistakes investors make is waiting until March to invest a lump sum. This can lead to liquidity issues and forces you to invest at whatever the market price is at that moment. By starting an SIP in an ELSS fund in April, you spread your investment over 12 months. This “rupee cost averaging” ensures you buy more units when prices are low and fewer when they are high, leading to better long-term results.

2. Matching Your Risk Profile

Not all ELSS funds are created equal. Some fund managers focus on large-cap stocks, which are relatively stable, while others might take higher exposure in mid-cap or small-cap stocks for higher growth. Before choosing a fund, analyze the underlying portfolio to ensure it aligns with your risk tolerance.

3. The “Roll-Over” Strategy

If you have a limited surplus for new investments, you can utilize the 3-year lock-in period to your advantage. Once your ELSS units complete three years, you can redeem them and reinvest the same amount back into an ELSS fund. This “recycling” allows you to claim a fresh tax deduction under Section 80C for the new financial year without actually committing fresh capital. However, be mindful of the tax on gains during redemption.

Taxability of ELSS Returns

While the investment is tax-deductible, it is important to understand how the returns are taxed. ELSS funds are treated as equity assets.

- Short-term Capital Gains (STCG): Since there is a 3-year lock-in, STCG is not applicable.

- Long-term Capital Gains (LTCG): Gains exceeding ₹1.25 lakh in a financial year are taxed at a rate of 12.5% (as per latest regulations). Despite this tax, the net returns from ELSS often remain higher than tax-free instruments like PPF due to equity growth.

Diversifying Beyond Section 80C

While Section 80C is the most popular, smart investors look at the broader picture of tax-efficient investing.

Solution-Oriented Funds: Retirement and Children’s Plans

Some mutual funds are specifically designed for long-term goals like retirement or a child’s education. While not all offer 80C benefits, they provide a disciplined structure. Retirement funds, in particular, can sometimes offer tax benefits depending on the specific structure approved by the government.

Tax Loss Harvesting

This is a strategy where you sell mutual fund units that are currently at a loss to offset the capital gains made from other investments. By booking a loss on paper, you reduce your net taxable gain, thereby lowering your overall tax outgo. You can immediately reinvest the proceeds to maintain your desired asset allocation.

How to Select the Right ELSS Fund

Performance Consistency

Don’t just look at the last one-year return. Check how the fund has performed over 5 and 10-year periods. A good fund is one that consistently outperforms its benchmark and its peers across different market cycles.

Fund Manager Experience

In equity investing, the expertise of the fund manager is crucial. Research the manager’s track record and their investment philosophy. Are they aggressive or conservative? Does their style suit your financial goals?

Expense Ratio

The expense ratio is the annual fee charged by the mutual fund house to manage your money. Even a 0.5% difference can significantly impact your final wealth over 15-20 years. Always compare the expense ratios of various ELSS funds and consider “Direct” plans over “Regular” plans to save on commissions.

Common Pitfalls to Avoid

Investing More Than Necessary in 80C

If your EPF (Employee Provident Fund) and Life Insurance premiums already total ₹1.2 lakh, you only need to invest ₹30,000 in ELSS to reach the ₹1.5 lakh limit. Investing more in ELSS is fine for wealth creation, but you won’t get additional tax benefits beyond the ceiling.

Ignoring the Lock-in Period

Remember that every SIP installment has its own 3-year lock-in period. If you start an SIP in January 2026, that specific installment can only be withdrawn after January 2029. Ensure you have an emergency fund elsewhere so you don’t feel trapped by the lock-in.

Conclusion

Tax saving through mutual funds is a journey of dual benefits: immediate tax relief and long-term wealth creation. By moving away from stagnant traditional savings and embracing ELSS and strategic mutual fund planning, you position yourself to benefit from India’s economic trajectory.

Start your tax planning today, automate it via SIPs, and consult a financial advisor to ensure your tax-saving strategy is perfectly aligned with your life goals.