Understanding Systematic Withdrawal Plans (SWP)

Discover how a Systematic Withdrawal Plan (SWP) can provide a steady monthly income from your mutual fund investments while offering superior tax benefits compared to FDs.

- NV Trends

- 6 min read

In the traditional Indian household, the dream of financial security often revolves around one thing: a steady monthly income. For decades, the Fixed Deposit (FD) has been the go-to instrument for this purpose. Senior citizens, specifically, have relied on the monthly interest payout from FDs to manage their kitchen expenses and medical bills. However, with falling interest rates and high inflation, the traditional FD is often not enough to maintain one’s lifestyle.

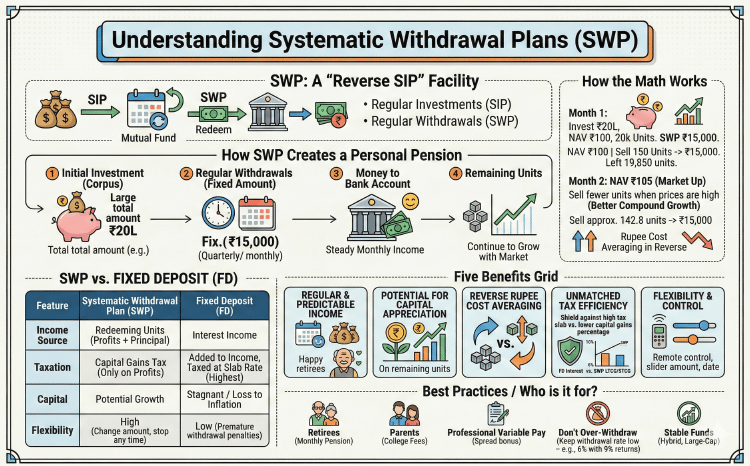

Enter the Systematic Withdrawal Plan, or SWP. If a Systematic Investment Plan (SIP) is about putting money into the market bit by bit to build wealth, an SWP is its mirror image. it is about taking money out of your investment bit by bit to create a personal pension.

What is a Systematic Withdrawal Plan (SWP)?

An SWP is a facility provided by mutual funds that allows an investor to withdraw a fixed amount of money at regular intervals (usually monthly, quarterly, or annually) from their existing mutual fund investment.

Think of it as a “reverse SIP.” Instead of the bank account being debited every month to buy units, the mutual fund house redeems (sells) a certain number of units from your portfolio and credits the money back to your bank account. The remaining units in your portfolio continue to grow, benefiting from market movements.

How Does the Math Work?

Let us say you have an investment of ₹20 Lakhs in a mutual fund and the current Net Asset Value (NAV) is ₹100. This means you own 20,000 units. You decide to start an SWP of ₹15,000 per month.

In the first month, if the NAV is ₹100, the fund house will sell 150 units (150 * 100 = 15,000) to give you your money. You are now left with 19,850 units.

In the second month, if the market goes up and the NAV becomes ₹105, the fund house only needs to sell approximately 142.8 units to give you the same ₹15,000. If the market goes down and the NAV is ₹95, they will sell about 157.9 units. This process continues until you stop the plan or the balance reaches zero.

Why Should You Consider an SWP?

1. Regular and Predictable Cash Flow

The biggest advantage is the certainty of income. Unlike dividends, which are at the discretion of the fund house and depend on distributable surplus, an SWP guarantees that the amount you requested will reach your bank account on the chosen date. This makes it ideal for retirees or anyone needing a secondary income stream.

2. Capital Appreciation Potential

While you are withdrawing a portion of your money, the remaining balance stays invested. If the fund’s rate of return is higher than the withdrawal rate, your capital can actually grow over time even while you are drawing an income. For example, if you withdraw 6% annually but the fund grows at 10%, your “corpus” (total value) increases.

3. Rupee Cost Averaging in Reverse

Just as SIP helps you buy more units when prices are low, SWP allows you to sell fewer units when the NAV is high. This keeps more units in your account during market rallies, allowing for better compounding on the remaining balance.

4. Unmatched Tax Efficiency

This is the “secret sauce” of SWP. In a Fixed Deposit, the entire interest you earn is added to your income and taxed at your slab rate (which could be as high as 30% plus cess).

In an SWP, you are not receiving “interest”; you are “redeeming units.” This is considered a capital gain. Only the profit component of the withdrawal is taxed, not the principal. Furthermore, if you hold equity-oriented funds for more than a year, the first ₹1.25 Lakh of long-term capital gains in a financial year is tax-free (as per 2024-25 rules). This makes the effective tax rate on SWP much lower than an FD.

SWP vs. Dividend Payout Option

Many investors get confused between the “IDCW” (Income Distribution cum Capital Withdrawal) option and an SWP. Here is why SWP is generally superior:

- Control: In IDCW, the AMC decides when and how much to pay. In SWP, you decide the amount and the date.

- Consistency: Dividends are not guaranteed. SWP is a contract to sell units, so the cash flow is guaranteed as long as there is a balance.

- Taxation: Dividends are taxed at your income tax slab rate. SWP withdrawals are taxed as capital gains, which is almost always cheaper for people in the 20% or 30% tax brackets.

Who is an SWP Best Suited For?

The Retiree

If you have a lump sum from your PF or Gratuity, putting it into a Conservative Hybrid or a Debt fund and starting an SWP can act as a monthly pension that beats inflation.

The Professional with Variable Pay

If you have a large bonus but want to spread it out to cover your monthly EMIs or lifestyle expenses, an SWP from a Liquid or Ultra Short-Term fund works perfectly.

Parents with Children in College

Instead of keeping a large amount in a savings account for a child’s 4-year degree expenses, you can keep it in a mutual fund and set an SWP to pay the quarterly fees and monthly allowance.

Taxation of SWP in India

Understanding the tax implications is vital for Indian investors. The tax depends on the type of fund you are withdrawing from:

Equity-Oriented Funds (More than 65% in Indian stocks)

- Short-Term (Held < 1 year): Gains are taxed at 20%.

- Long-Term (Held > 1 year): Gains up to ₹1.25 Lakh per year are exempt. Gains above this are taxed at 12.5%.

Debt-Oriented Funds

- Investments made after April 1, 2023: All gains are added to your income and taxed at your slab rate, regardless of the holding period.

Best Practices for a Successful SWP

- Don’t Over-Withdraw: A healthy thumb rule is to keep your withdrawal rate lower than the expected long-term return of the fund. If a fund expects to return 9%, try to keep your SWP at 6-7% to ensure your capital doesn’t erode.

- Choose the Right Asset Class: Do not do an SWP from a highly volatile Small-cap fund if you depend on that money for survival. Use Hybrid funds or Large-cap funds which are relatively more stable.

- Wait for a Year (if possible): To take advantage of Long-Term Capital Gains tax benefits in equity funds, try to start your SWP one year after the initial investment.

Key Takeaways

- Reliable Income: SWP provides a fixed, regular cash flow, making it an excellent tool for retirement.

- Tax Advantage: It is significantly more tax-efficient than Fixed Deposits or Dividend options because only the “gain” part is taxed at capital gains rates.

- Flexibility: You can start, stop, or change the withdrawal amount at any time without any penalties in most cases.

- Growth Potential: Unlike an annuity where your capital is gone, in an SWP, the remaining units continue to grow and remain accessible to you in case of emergencies.

Conclusion

The Systematic Withdrawal Plan is perhaps the most underutilized tool in the Indian financial landscape. While we have embraced SIPs for building wealth, we are yet to fully appreciate SWPs for consuming wealth smartly. Whether you are looking for a retirement pension or just a way to manage your monthly expenses more efficiently, the SWP offers a blend of flexibility, growth, and tax-saving that traditional instruments simply cannot match.

Before starting, consult with a financial advisor to determine the right withdrawal rate and the most suitable funds for your specific goals.