Understanding Risk and Return in Mutual Funds

Master the fundamentals of the risk-return tradeoff in mutual funds to build a stronger, more balanced investment portfolio in the Indian market.

- NV Trends

- 6 min read

When it comes to investing in India, the most common question asked at dinner tables or office breaks is: “Kitna return milega?” (How much return will I get?). While everyone loves the idea of doubling their money, few stop to ask about the other side of the coin: the risk. In the world of mutual funds, risk and return are like two sides of the same rupee note; you cannot have one without the other.

Understanding the relationship between risk and return is the cornerstone of successful investing. Whether you are a conservative investor looking to beat inflation or an aggressive one aiming for long-term wealth creation, knowing how to balance these two factors will define your financial journey.

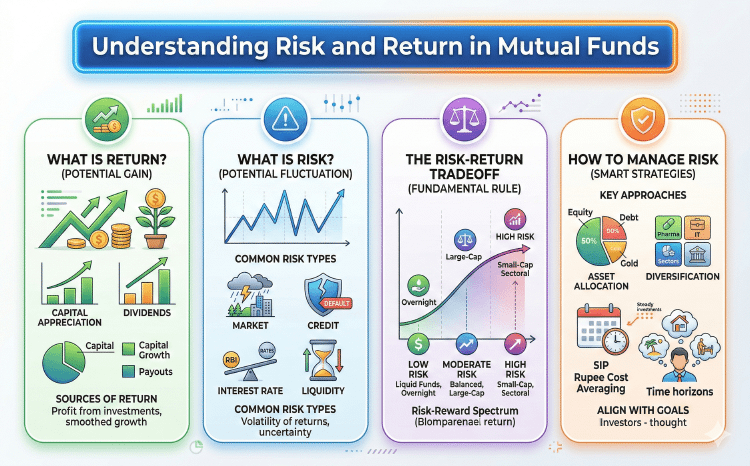

What is Return in Mutual Funds?

In simple terms, return is the profit or gain you make on your investment over a period of time. In mutual funds, returns are usually generated through capital appreciation (increase in the price of the fund units) or dividends.

Types of Returns You Should Know

To compare funds effectively, you need to understand how returns are calculated:

- Absolute Returns: This is the simple percentage increase in your investment. If you invested ₹1 Lakh and it grew to ₹1.10 Lakh, your absolute return is 10%. This is useful for short-term periods (less than a year).

- CAGR (Compounded Annual Growth Rate): This represents the mean annual growth rate of an investment over a period longer than one year. It smooths out the volatility and shows what you earned annually on a compounded basis.

- XIRR (Extended Internal Rate of Return): If you are investing via a Systematic Investment Plan (SIP), XIRR is the most accurate measure. It accounts for multiple cash flows occurring at different points in time.

What is Risk in Mutual Funds?

Risk is often misunderstood as simply “losing money.” While that is the ultimate risk, in financial terms, risk refers to the volatility or the uncertainty of the returns. It is the possibility that the actual return will be different from the expected return.

Common Types of Risks in the Indian Market

Investors in India face several specific types of risks:

- Market Risk: Also known as systematic risk, this is the risk of the entire market going down due to economic factors, political instability, or global events. If the Nifty or Sensex crashes, most equity funds will see a dip.

- Credit Risk: Mainly applicable to debt funds, this is the risk that the company or entity that borrowed money (by issuing bonds) fails to pay back the interest or the principal.

- Interest Rate Risk: When interest rates in the economy rise, bond prices fall, and vice versa. This affects the Net Asset Value (NAV) of debt mutual funds.

- Liquidity Risk: The risk that a fund manager might not be able to sell certain securities in the portfolio quickly enough to meet redemption requests without taking a loss.

The Risk-Return Tradeoff

The fundamental rule of finance is the risk-return tradeoff. It states that the potential return rises with an increase in risk.

If you want the safety of a Government Bond or a Fixed Deposit (FD), you must accept lower returns. If you want the high returns associated with small-cap stocks, you must be prepared for significant price swings and the possibility of short-term losses.

Visualizing the Spectrum

- Low Risk / Low Return: Liquid Funds, Overnight Funds.

- Moderate Risk / Moderate Return: Balanced Advantage Funds, Hybrid Funds, Large-cap Equity Funds.

- High Risk / High Return: Sectoral Funds, Small-cap Funds, Mid-cap Funds.

Measuring Risk: Tools for the Smart Investor

How do you know if a fund is “too risky”? You don’t have to guess. There are several statistical measures used by analysts in India to quantify risk:

Standard Deviation

This measures how much the fund’s return fluctuates from its average return. A high standard deviation means the fund is more volatile. If you prefer a “smooth ride,” look for funds with lower standard deviation in their category.

Beta

Beta measures a fund’s sensitivity to market movements. A Beta of 1.0 means the fund moves in line with its benchmark (like the Nifty 50). A Beta of 1.2 suggests the fund is 20% more volatile than the market, while a Beta of 0.8 means it is 20% less volatile.

Sharpe Ratio

This is one of the most important metrics. It tells you how much “excess return” you are getting for the extra risk you are taking. A higher Sharpe Ratio indicates that the fund manager is delivering better returns for every unit of risk involved.

How to Manage Risk in Your Portfolio

You cannot eliminate risk entirely, but you can certainly manage it. Here are some strategies tailored for Indian investors:

1. Asset Allocation

Don’t put all your eggs in one basket. Spread your money across equity, debt, and gold. When the stock market is volatile, your debt and gold investments provide stability to the overall portfolio.

2. Diversification

Even within equity, diversify across different sectors (Banking, IT, Pharma, Consumption) and market caps (Large, Mid, Small). This ensures that a slump in one industry doesn’t wipe out your entire gain.

3. Use the Power of SIP

The Systematic Investment Plan (SIP) is a great risk-mitigation tool. By investing a fixed amount every month, you buy more units when prices are low and fewer units when prices are high. This averages out the cost of your investment over time, reducing the impact of market volatility.

4. Align with Financial Goals

Risk is subjective. If you are saving for a vacation next year, you shouldn’t be in equity funds (High Risk). However, if you are saving for retirement 20 years away, the short-term volatility of equity is a risk you can afford to take for the higher long-term reward.

Key Takeaways

- No Risk, No Gain: Every mutual fund carries some level of risk; even “safe” debt funds are subject to interest rate and credit risks.

- Understand the Metric: Use Beta and Sharpe Ratio to compare funds within the same category to see which one manages risk better.

- Time Horizon is Key: High-risk funds require a longer time horizon (5-7+ years) to allow volatility to smooth out.

- Diversification is Your Friend: A well-balanced portfolio across asset classes is the best defense against market uncertainty.

- Consistency Matters: Instead of trying to time the market (which is risky), stay invested through SIPs to benefit from rupee cost averaging.

Conclusion

Investing in mutual funds without understanding risk is like driving a car without knowing where the brakes are. While the allure of high returns is strong, your primary goal should be to stay in the game. By choosing funds that align with your risk tolerance and financial goals, you can navigate the ups and downs of the Indian market with confidence.

Remember, the “best” fund is not necessarily the one with the highest return last year, but the one that gives you the best return for the level of risk you are comfortable taking. Happy investing!