Retirement Planning Using Mutual Funds

Secure your future with a comprehensive guide to retirement planning using mutual funds in India. Learn about asset allocation, SIPs, and long-term wealth creation.

- NV Trends

- 5 min read

Retirement is a phase of life that most of us look forward to, yet few of us adequately prepare for. In the Indian context, the traditional safety nets are changing. With the decline of joint family systems and the absence of a universal social security pension for the private sector, the responsibility of building a retirement nest egg falls squarely on the individual. The good news? Mutual funds offer one of the most flexible and powerful tools to achieve a dignified and financially independent retirement.

Why Retirement Planning is Essential Today

For many young professionals in India, retirement seems like a distant reality. However, starting early is the single most important factor in successful financial planning. With increasing life expectancy and rising healthcare costs, your retirement corpus needs to last much longer than it did for previous generations.

Inflation is the silent killer of purchasing power. A monthly expense of ₹50,000 today could easily escalate to ₹2,00,000 in twenty years, assuming a 7% inflation rate. If your savings are parked in traditional low-yield instruments, you might find your corpus exhausted much sooner than expected. This is where mutual funds come into play, offering the potential for inflation-beating returns over the long term.

The Role of Mutual Funds in Your Retirement Journey

Mutual funds are not a “one-size-fits-all” solution. They provide a spectrum of options that can be tailored to your age, risk appetite, and time horizon. By investing in a diversified basket of stocks, bonds, or a mix of both, you can participate in the growth of the Indian economy while managing your risks.

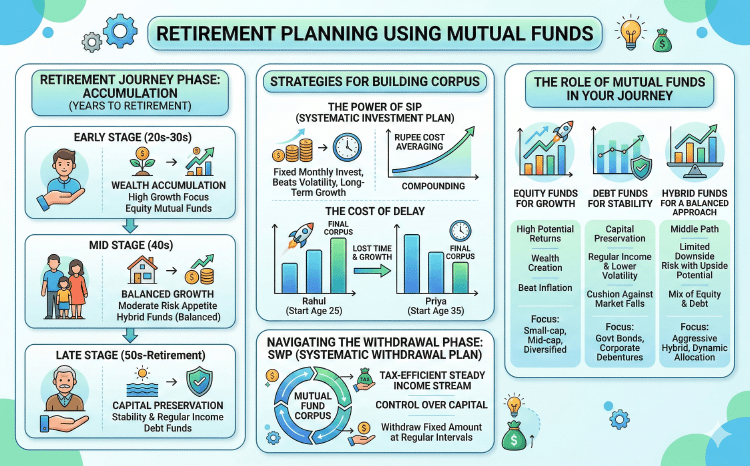

Equity Mutual Funds for Growth

When you are 20 or 30 years away from retirement, your primary goal is wealth accumulation. Equity mutual funds are ideal for this stage because they have the potential to deliver high returns over the long run. By investing in diversified equity funds, large-cap funds, or mid-cap funds, you allow your money to benefit from the power of compounding.

Debt Mutual Funds for Stability

As you get closer to your retirement age, the focus shifts from aggressive growth to capital preservation. Debt funds invest in fixed-income securities like government bonds and corporate debentures. They provide a cushion against the volatility of the stock market and ensure that your accumulated wealth is relatively safe.

Hybrid Funds for a Balanced Approach

For those who prefer a “middle path,” hybrid funds (or balanced funds) invest in both equity and debt. These are excellent for investors who want some exposure to the stock market’s upside but want to limit the downside risk through debt allocation.

Strategies for Building a Retirement Corpus

The Power of the Systematic Investment Plan (SIP)

In India, the SIP has become synonymous with disciplined investing. For retirement planning, the SIP is your best friend. It allows you to invest a fixed amount every month, regardless of market conditions. This strategy, known as Rupee Cost Averaging, ensures that you buy more units when the market is low and fewer units when it is high. Over decades, this significantly reduces the average cost of your investment.

Starting Early: The Cost of Delay

Consider two friends, Rahul and Priya. Rahul starts an SIP of ₹10,000 at age 25. Priya starts the same SIP at age 35. By the time they both reach 60, Rahul’s corpus will be significantly larger than Priya’s, even though Priya only delayed by ten years. This is because Rahul’s money had an extra decade to compound. In retirement planning, time is more valuable than the amount you invest.

Step-Up SIPs

As your income grows, your investments should too. A Step-Up SIP allows you to increase your monthly contribution by a fixed percentage or amount every year. This small annual increase can have a massive impact on the final retirement corpus, helping you keep pace with your evolving lifestyle.

Navigating the Withdrawal Phase: SWP

The biggest worry for retirees is how to get a regular income from their accumulated corpus without exhausting it. This is where the Systematic Withdrawal Plan (SWP) comes in. An SWP allows you to withdraw a fixed amount from your mutual fund investment at regular intervals (monthly, quarterly, or annually).

Unlike a traditional pension, an SWP gives you control over your capital. You only pay tax on the capital gains portion of the withdrawal, making it a very tax-efficient way to generate retirement income in India compared to interest from Fixed Deposits.

Tax Implications to Consider

Understanding the tax rules is vital for maximizing your retirement returns.

- Equity Funds: Long-term capital gains (LTCG) over ₹1.25 lakh in a financial year are currently taxed at 12.5% (if held for more than a year). Short-term gains are taxed at 20%.

- Debt Funds: Gains from debt funds are generally added to your income and taxed according to your applicable income tax slab.

Strategic planning can help you minimize your tax outflow during both the accumulation and withdrawal phases.

Key Takeaways

- Start Now: The earlier you begin, the less you need to save monthly to reach your goal.

- Beat Inflation: Equity mutual funds are essential to ensure your corpus doesn’t lose value over time due to rising prices.

- Diversify: Use a mix of equity and debt funds based on your age and risk tolerance.

- Be Consistent: Stick to your SIPs even during market downturns; volatility is a long-term investor’s friend.

- Review Regularly: At least once a year, check if your portfolio is on track and rebalance if your asset allocation has drifted.

- Plan the Exit: Use SWPs for a tax-efficient, steady income stream during your golden years.

Conclusion

Retirement planning is not about hitting a specific number; it is about ensuring that you can maintain your lifestyle and dignity when you are no longer earning a monthly salary. Mutual funds provide the most transparent, liquid, and efficient vehicle for Indian investors to build this future.

By combining the discipline of SIPs with a smart asset allocation strategy, you can transform your retirement dreams into a reality. Remember, the best time to start was yesterday; the second best time is today. Consult with a financial advisor to create a personalized roadmap that aligns with your specific needs and family goals.