How to Rebalance Your Investment Portfolio

Learn the essential steps to rebalance your investment portfolio effectively to manage risk and maintain your long-term financial goals in the Indian market.

- NV Trends

- 6 min read

In the world of investing, there is a common phrase we often hear: “Set it and forget it.” While this sounds like a relaxing way to manage your money, the reality of the financial markets is quite different. Imagine planting a beautiful garden where you put roses in one corner and sunflowers in another. Over time, if left unattended, the sunflowers might grow too tall and shade the roses, or weeds might take over a specific patch. Your investment portfolio is very similar to that garden.

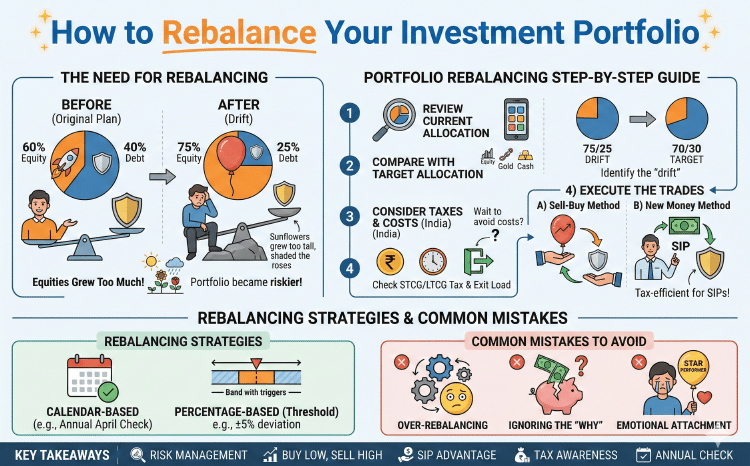

When you first start your investment journey in India, you likely decide on an asset allocation—perhaps 60% in equity mutual funds for growth and 40% in debt funds for safety. However, because markets move constantly, these percentages change. One year the stock market might perform exceptionally well, pushing your equity portion to 75%. While this looks like a gain, it also means your portfolio is now much riskier than you originally intended. This is where the crucial process of rebalancing comes into play.

What is Portfolio Rebalancing?

Portfolio rebalancing is the process of bringing your investment portfolio back to its original target asset allocation. It involves selling a portion of the assets that have performed well and buying more of the assets that have underperformed or remained stagnant.

For many Indian investors, the idea of selling something that is making money (like a high-performing equity fund) to buy something that isn’t (like a slow-moving debt fund) feels counterintuitive. However, rebalancing is not about chasing the highest returns; it is fundamentally about risk management. It ensures that you are not overexposed to a single asset class when market conditions eventually change.

Why is Rebalancing Important for Indian Investors?

The Indian market is known for its volatility. We see periods of rapid “bull runs” where mid-cap and small-cap funds skyrocket, followed by periods of “bear markets” or sideways movement. Without rebalancing, your portfolio becomes a slave to market movements.

1. Controlling Risk

If your equity allocation grows from 50% to 80% during a market boom, a 20% market correction will hit your total wealth much harder than it would have at your original 50% allocation. Rebalancing forces you to take “chips off the table” when prices are high, protecting your capital.

2. Buying Low and Selling High

Rebalancing automatically enforces the golden rule of investing. When you rebalance, you are selling assets that have become expensive (high) and buying assets that are relatively cheaper (low). This disciplined approach removes emotion from the decision-making process.

3. Staying Aligned with Goals

Every investment should be tied to a financial goal, such as a child’s education or your retirement. As you get closer to these goals, your ability to take risks decreases. Rebalancing helps you gradually shift from aggressive assets to safer ones as your deadline approaches.

When Should You Rebalance?

There are generally two popular strategies for timing your rebalancing:

The Calendar-Based Approach

This involves checking your portfolio at fixed intervals—usually once a year or every six months. For example, every April (the start of the Indian financial year), you review your holdings. If your 60/40 split has become 65/35, you make the necessary trades. This is the simplest method and requires the least amount of monitoring.

The Percentage-Based (Threshold) Approach

In this method, you only rebalance when an asset class moves beyond a specific “trigger” or “band.” For instance, if you allow a 5% deviation, you only take action if your equity moves above 65% or below 55%. This is more responsive to market conditions but requires you to keep a closer eye on your portfolio.

Step-by-Step Guide to Rebalancing Your Portfolio

Step 1: Review Your Current Allocation

The first step is to log into your investment portals or apps and calculate the current market value of all your holdings. Group them into categories: Equity, Debt, Gold, and Cash. Calculate what percentage of your total wealth each category currently represents.

Step 2: Compare with Your Target Allocation

Look back at your original plan. If your plan was 70% Equity and 30% Debt, but your current reality is 78% Equity and 22% Debt, you have identified a “drift.” You now know exactly how much you need to move to get back to your target.

Step 3: Consider Taxes and Exit Loads

Before you start selling, you must be aware of the costs. In India, selling equity mutual funds within one year usually attracts Short-Term Capital Gains (STCG) tax of 20%, while holding for more than a year incurs Long-Term Capital Gains (LTCG) tax of 12.5% (on gains above ₹1.25 lakh). Additionally, many funds have an “exit load” (usually 1%) if you sell within a year. Sometimes, it is better to wait a few weeks to avoid these costs.

Step 4: Execute the Trades

There are two ways to rebalance:

- The Sell-Buy Method: Sell the over-performing asset and use the proceeds to buy the under-performing one.

- The New Money Method: Instead of selling, use your fresh monthly investments (or SIPs) to buy only the under-performing asset until the balance is restored. This is often the most tax-efficient way for salaried individuals.

Common Mistakes to Avoid

Over-Rebalancing

Don’t try to rebalance every time the market moves 1%. Frequent trading leads to higher brokerage costs, taxes, and unnecessary stress. Once or twice a year is usually sufficient for most retail investors.

Ignoring the “Why”

Sometimes an asset class underperforms because of a fundamental change, not just market cycles. Before buying more of an under-performing fund, ensure that its long-term potential is still intact and that you aren’t just “throwing good money after bad.”

Emotional Attachment

It is hard to sell a “star performer.” Many investors feel they are “punishing” their best funds by selling them. Remember, rebalancing is a mathematical necessity to keep your risk in check, not a judgment on the fund’s quality.

Key Takeaways

- Risk Management over Returns: Rebalancing is primarily about keeping your portfolio’s risk level consistent with your comfort zone.

- Automatic Discipline: It forces you to sell high and buy low without letting greed or fear get in the way.

- Tax Awareness: Always calculate the impact of Capital Gains Tax and Exit Loads before selling your investments in India.

- Frequency: For most people, a simple annual check-up is the best way to maintain a healthy portfolio.

- The SIP Advantage: You can often rebalance by simply redirecting your future SIPs into the asset class that is currently lagging.

Conclusion

Rebalancing is the secret weapon of successful long-term investors. While it might not seem exciting during a massive bull market, it is the very action that saves your portfolio during a crash. By treating your investments like a garden—regularly pruning the overgrowth and nourishing the thirsty areas—you ensure that your financial future remains healthy and vibrant.

Start by looking at your portfolio today. Is it still the same “garden” you intended to plant, or has the market turned it into something else? A little bit of maintenance today can lead to a much more secure tomorrow.