How to Read Mutual Fund NAVs Effectively

Learn how to interpret Mutual Fund Net Asset Value (NAV) correctly to make better investment decisions in the Indian market.

- NV Trends

- 6 min read

For many new investors in India, the world of mutual funds often begins and ends with one three-letter acronym: NAV. You see it on financial news websites, in your monthly account statements, and on every investment app. However, there is a common misconception that a lower NAV makes a fund “cheaper” or a better deal, similar to how a low stock price might attract value investors.

Understanding what Net Asset Value (NAV) actually represents—and more importantly, what it doesn’t—is crucial for managing your portfolio effectively. In this guide, we will break down the complexities of NAV into simple terms to help you become a more informed investor.

What Exactly is Mutual Fund NAV?

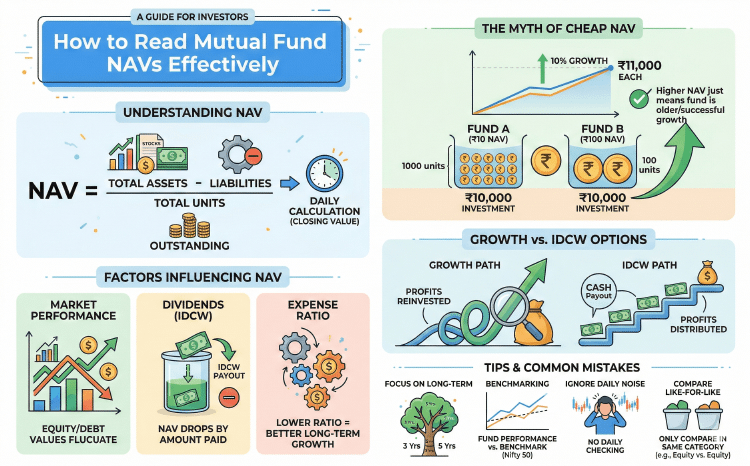

Net Asset Value (NAV) represents the market value per unit of a mutual fund scheme. Think of it as the book value of a single unit. It is calculated by taking the total value of all the cash and securities in the fund’s portfolio, subtracting any liabilities (like management fees and operational expenses), and then dividing that number by the total number of units outstanding.

In India, Asset Management Companies (AMCs) calculate and publish the NAV of their schemes at the close of every business day. This is different from stocks, where the price changes every second during market hours.

The Myth of the “Cheap” NAV

One of the most persistent myths in Indian retail investing is that a fund with an NAV of ₹10 is better than a fund with an NAV of ₹100 because you get “more units.”

Let’s look at a simple example. Suppose you invest ₹10,000 in two different funds, Fund A and Fund B. Both funds invest in the exact same set of stocks and perform identically.

- Fund A: NAV is ₹10. You get 1,000 units.

- Fund B: NAV is ₹100. You get 100 units.

If both funds grow by 10%, your investment in Fund A is now worth ₹11,000, and your investment in Fund B is also worth ₹11,000. The number of units you hold is irrelevant to the growth of your capital. The NAV is simply a reflection of how long the fund has been running and its historical growth. A higher NAV often just means the fund has been around longer and has successfully grown its assets over time.

Key Takeaways

- NAV is the market value of a single unit of a mutual fund.

- It is calculated daily after the market closes.

- A lower NAV does not mean a fund is “cheap” or “undervalued.”

- Performance should be judged by the percentage growth of NAV, not its absolute value.

- NAV is net of the expense ratio, meaning the costs are already deducted.

Factors That Influence NAV Movement

The NAV of your mutual fund is not a static number; it fluctuates based on several internal and external factors. Understanding these will help you read your statements with more clarity.

1. Market Performance of Underlying Assets

This is the most significant factor. If you are invested in an equity fund, your NAV will rise and fall based on the stock prices of the companies the fund owns. For debt funds, the NAV is influenced by interest rate movements and the credit quality of the bonds held in the portfolio.

2. Dividends and Distributions

When a mutual fund pays out a dividend (under the Income Distribution cum Capital Withdrawal or IDCW option), the NAV of the fund drops by the amount of the dividend paid. This is because money is leaving the fund’s pool to be paid to investors.

3. Expense Ratio

Managing a fund costs money. There are salaries for fund managers, administrative costs, and marketing expenses. These are represented by the expense ratio. Since the NAV is calculated after subtracting these liabilities, a lower expense ratio generally leads to a slightly higher NAV growth over time compared to a similar fund with higher costs.

NAV and the Impact of Entry and Exit Timing

In India, the timing of your purchase or redemption request determines the NAV you receive. This is known as “Cut-off Timing.”

- Purchases: If you submit your application and the funds reach the AMC before the cut-off time (usually 3:00 PM), you get the NAV of that same day. If you miss the cut-off, you get the next business day’s NAV.

- Redemptions: Similarly, if you put in a request to sell your units before the cut-off, you get that day’s closing NAV.

For long-term investors, the daily fluctuation of a few paise in the NAV shouldn’t be a major concern, but it is good to know how the mechanism works.

How to Use NAV to Track Performance

While the absolute value of the NAV isn’t a great indicator of a fund’s quality, the change in NAV over time is the best way to track performance.

Cumulative Returns

Compare the NAV of today with the NAV from one, three, or five years ago. This gives you the total percentage growth. In India, most platforms show “Point-to-Point” returns based on these NAV changes.

Benchmarking

Always compare the NAV growth of your fund against its benchmark (like the Nifty 50 or S&P BSE 200). If the benchmark grew by 15% and your fund’s NAV only grew by 10%, the fund manager is underperforming, regardless of how high the absolute NAV is.

The Difference Between Growth and IDCW (Dividend) NAVs

When looking at a fund’s factsheet, you will often see different NAVs for the ‘Growth’ option and the ‘IDCW’ (formerly Dividend) option.

- Growth Option: All profits made by the fund are reinvested. This leads to a compounding effect and a much higher NAV over the long term.

- IDCW Option: Part of the profits are paid out to the investor. As mentioned earlier, every time a payout happens, the NAV drops.

For most individual investors in India looking to build wealth, the Growth option is generally recommended because it allows the NAV to grow unhindered.

Common Mistakes When Reading NAVs

Focusing on Short-term Fluctuations

The Indian market can be volatile. Looking at your NAV every day can lead to emotional decisions. It is better to review the NAV trends quarterly or annually.

Ignoring the Impact of Taxes

When you see your NAV has increased, remember that this represents “unrealized gains.” When you sell your units, you will be liable for Capital Gains Tax. In 2026, the tax rules for equity and debt funds are specific, so your “in-hand” value will be slightly less than the NAV multiplied by your units.

Comparing NAVs Across Different Categories

You cannot compare the NAV of a Liquid Fund with that of a Small-Cap Fund. They have different risk profiles, different asset classes, and different objectives. Only compare NAV growth between funds in the same category.

Conclusion

Reading mutual fund NAVs effectively is about looking beyond the surface number. It is a tool for transparency, allowing you to see exactly what your portion of the fund is worth at the end of every day. By ignoring the myth of “cheap” NAVs and focusing on consistent percentage growth and benchmark comparison, you can make smarter choices for your financial future.

Whether you are a seasoned investor or just starting your first SIP, keep your eyes on the long-term trajectory of the NAV rather than the daily noise. Your goal is not to buy a “low price” unit, but to own a piece of a “high quality” portfolio.