Understanding Expense Ratios in Mutual Funds

Learn everything about mutual fund expense ratios in India, how they impact your long-term wealth, and how to choose the right fund for better returns.

- NV Trends

- 6 min read

When we talk about investing in mutual funds in India, most of our attention goes toward the potential returns. We look at the “star ratings,” the past three-year performance, and the fund manager’s reputation. However, there is a silent factor that works behind the scenes, constantly eating away a small portion of your investment every single day. This factor is the Expense Ratio.

If you want to build significant wealth over 10, 15, or 20 years, understanding the expense ratio is not just optional—it is essential. A difference of just 1% in fees might seem tiny today, but over a long investment horizon, it can translate into a difference of lakhs of rupees in your final corpus.

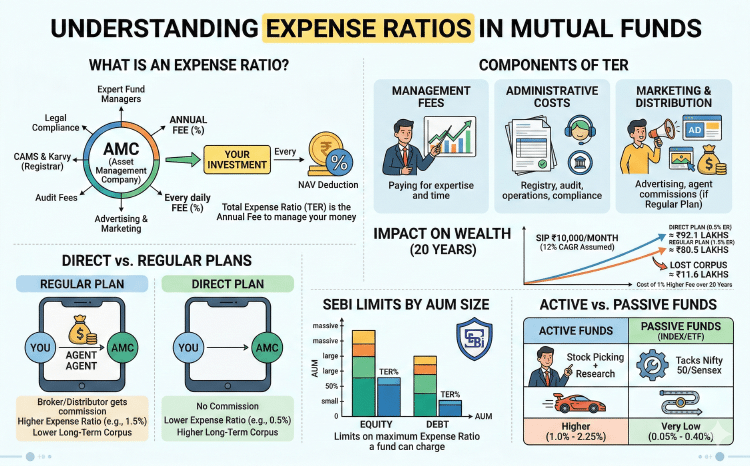

What is an Expense Ratio?

In simple terms, an Asset Management Company (AMC) or a mutual fund house is a business. To manage your money, they hire expert fund managers, maintain offices, pay for legal compliance, conduct research, and market their products. All these activities cost money.

The expense ratio is the annual fee that a mutual fund charges its unit holders to cover these operational costs. It is expressed as a percentage of the fund’s daily net assets. For example, if you invest ₹1,00,000 in a fund with an expense ratio of 1.5%, you are essentially paying ₹1,500 annually to the AMC to manage your money.

The important thing to remember is that the Net Asset Value (NAV) reported by the fund house is already “net of expenses.” This means the fee is deducted daily before the NAV is declared, so you don’t receive a separate bill for it.

Components of the Expense Ratio

What exactly are you paying for when you see that percentage? The Total Expense Ratio (TER) typically includes:

1. Management Fees

This is the largest component. It goes toward paying the fund manager and the investment team who decide which stocks or bonds to buy and sell. You are paying for their expertise and time.

2. Administrative Costs

Running a mutual fund involves a lot of paperwork, customer service, registry fees (like CAMS or Karvy), and audit fees. These costs ensure that the fund operates legally and transparently.

3. Marketing and Distribution Expenses

Fund houses spend money to reach new investors. This includes advertising and commissions paid to distributors or brokers who sell the funds to retail investors.

Direct vs. Regular Plans: The Big Difference

In India, every mutual fund scheme has two versions: a Regular Plan and a Direct Plan. The primary difference between the two is the expense ratio.

- Regular Plan: You buy this through a broker, agent, or distributor. The AMC pays a commission to this intermediary, which is added to the expense ratio. Consequently, the expense ratio is higher.

- Direct Plan: You buy this directly from the AMC’s website or app. Since there is no intermediary, there is no commission. The expense ratio is significantly lower, often by 0.5% to 1.0%.

Over the long term, the compounded effect of saving that 1% every year in a Direct Plan leads to a much higher final balance.

The Impact of High Expenses on Your Wealth

Many Indian investors ignore the expense ratio because it feels like a small number. Let’s look at a practical example to see why this is a mistake.

Suppose you start an SIP of ₹10,000 per month for 20 years. We assume the underlying market returns are 12% per year.

- Scenario A (Direct Plan): Expense ratio is 0.5%. Your net return is 11.5%. After 20 years, your corpus is approximately ₹92.1 Lakhs.

- Scenario B (Regular Plan): Expense ratio is 1.5%. Your net return is 10.5%. After 20 years, your corpus is approximately ₹80.5 Lakhs.

By choosing the plan with the higher expense ratio, you lost nearly ₹11.6 Lakhs! That is the “cost” of a 1% higher fee. It highlights why cost-effective investing is the secret to long-term success.

SEBI Limits on Expense Ratios

The Securities and Exchange Board of India (SEBI) is the watchdog of the Indian financial markets. To protect retail investors, SEBI has capped the maximum expense ratio an AMC can charge.

The limits are based on the Assets Under Management (AUM) of the scheme. Generally, as the fund grows larger (higher AUM), the AMC must reduce the expense ratio. This is because the fixed costs of managing a fund (like the manager’s salary) get spread over a larger pool of money, making it more efficient.

For equity-oriented schemes, the TER can range from roughly 2.25% for small funds down to much lower percentages for massive funds. For debt funds, the limits are even lower.

Active vs. Passive Funds: The Cost Battle

When choosing a fund, you will encounter two styles:

Active Funds

These are funds where the manager tries to beat the market index (like the Nifty 50) by picking specific stocks. Because of the high level of research and management involved, active funds have higher expense ratios (usually 1% to 2.25%).

Passive Funds (Index Funds/ETFs)

These funds simply track an index. There is no “stock picking” involved. Since the management is automated and simple, the expense ratios are very low, often between 0.05% and 0.40%. In recent years, many Indian investors have moved toward Index Funds because it is difficult for active managers to consistently beat the index after accounting for their high fees.

How to Check the Expense Ratio

Before you invest, you can easily find the expense ratio on:

- The AMC’s official website.

- The Scheme Information Document (SID) or Key Information Memorandum (KIM).

- Popular mutual fund research platforms and apps.

- The monthly “Fact Sheet” published by the fund house.

Always compare the expense ratio of a fund with its “Category Average.” If a fund is charging much more than its peers, it must justify that cost with significantly better performance.

Key Takeaways

- It is a Recurring Cost: The expense ratio is charged every year, regardless of whether the fund makes a profit or a loss.

- Lower is Usually Better: All other things being equal, a lower expense ratio leads to higher net returns for the investor.

- Direct Plans are Winners: If you are comfortable managing your own investments, always opt for Direct Plans to save on commission costs.

- Size Matters: Larger funds usually have lower expense ratios due to SEBI’s tiered pricing structure.

- Passive Investing is Cheaper: If you want to keep costs to an absolute minimum, look into Index Funds and ETFs.

- Don’t Ignore Performance: While cost is important, don’t choose a bad fund just because it is cheap. The goal is to find the best balance between performance and cost.

Conclusion

The expense ratio might look like a footnote in a mutual fund brochure, but it is one of the most powerful predictors of your long-term investment success. In the Indian market, where competition is high and market alpha (excess return) is shrinking, every rupee saved in fees is a rupee earned in returns.

Next time you review your portfolio, take a close look at the “TER” column. If you are paying too much for mediocre performance, it might be time to switch to a more cost-effective plan or an index fund. Remember, in the world of compounding, even the smallest leak can sink a big ship over time.