How to Evaluate Fund Manager Performance

Learn the essential metrics and qualitative factors to effectively evaluate a mutual fund manager’s performance and make informed investment decisions in India.

- NV Trends

- 6 min read

In the Indian mutual fund industry, while we often talk about expense ratios, NAVs, and historical returns, we frequently overlook the “pilot” of the ship: the Fund Manager. When you invest in an actively managed mutual fund, you are essentially hiring a professional to make complex financial decisions on your behalf. Whether the fund beats the market or lags behind depends heavily on the skill, strategy, and discipline of this individual or team.

Evaluating a fund manager is not just about looking at the latest one-year return. It requires a deeper dive into how those returns were achieved and whether the manager can replicate that success in different market conditions. This guide will walk you through the quantitative and qualitative aspects of evaluating fund manager performance in the Indian context.

Why the Fund Manager Matters

In passive funds like Index Funds or ETFs, the manager’s role is minimal—they simply track an index like the Nifty 50. However, in active funds (Small-cap, Mid-cap, Flexi-cap, etc.), the manager has the liberty to pick specific stocks and exit others. A skilled manager can identify “multi-bagger” stocks before they become popular, whereas an unskilled one might hold onto “value traps” that drain your portfolio.

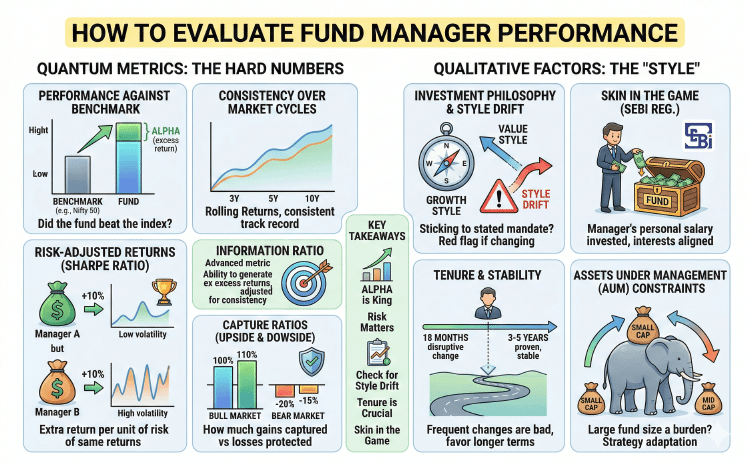

Quantitative Metrics: The Hard Numbers

To move beyond “gut feeling,” investors should use specific statistical tools to measure a manager’s efficiency.

1. Performance Against the Benchmark

The first rule of evaluation is comparing the fund’s return against its benchmark. If a Large-cap fund returns 12% but the Nifty 50 TRI returned 15% in the same period, the manager has underperformed. A good manager should consistently deliver “Alpha”—which is the excess return generated over the benchmark.

2. Consistency Over Multiple Market Cycles

A “one-hit wonder” can happen in the stock market. A manager might get lucky with one sector bet during a bull run. The real test is consistency. Look at 3-year, 5-year, and 10-year rolling returns. Rolling returns provide a clearer picture of how the manager performed across various starting and ending points, smoothing out the bias of a specific “good year.”

3. Risk-Adjusted Returns (Sharpe Ratio)

High returns are great, but did the manager take excessive risks to get them? The Sharpe Ratio measures how much extra return you get for every unit of risk taken. If two managers both delivered 15% returns, but Manager A did it with much lower volatility (lower risk) than Manager B, then Manager A is the superior performer.

4. Information Ratio

This is a more advanced metric that specifically evaluates the manager’s ability to generate excess returns relative to the benchmark, adjusted for the consistency of that excess return. A higher Information Ratio indicates a manager who consistently beats the benchmark without taking wild, erratic bets.

5. Capture Ratios (Upside and Downside)

- Upside Capture Ratio: Shows how much of the market’s gains the manager captured during a bull phase.

- Downside Capture Ratio: Shows how much the fund fell when the market crashed. A stellar manager typically has an upside capture ratio of over 100% and a downside capture ratio of less than 80-90%. In India, protecting the downside is often more important for long-term wealth than chasing every bit of the upside.

Qualitative Factors: The “Style” of the Manager

Numbers tell you what happened; qualitative analysis tells you how it happened and if it might continue.

1. Investment Philosophy and Style Drift

Does the manager follow a “Value” style or a “Growth” style? Evaluation involves checking if the manager sticks to their stated mandate. If a “Value” manager starts buying expensive, high-momentum stocks just to boost short-term performance, it is called “Style Drift.” This is a red flag, as it shows a lack of conviction in their core strategy.

2. Skin in the Game

SEBI (Securities and Exchange Board of India) now requires fund managers to invest a portion of their salary into the schemes they manage. When a manager has their own hard-earned money in the fund, their interests are perfectly aligned with yours. You can check these disclosures in the fund’s monthly fact sheets.

3. Tenure and Stability

Frequent changes in fund management can be disruptive. It takes time for a manager to build a portfolio and for their thesis to play out. If a fund changes its manager every 18 months, it becomes difficult to attribute performance to any single individual. Look for managers who have been at the helm for at least 3 to 5 years.

4. Assets Under Management (AUM) Constraints

In the Indian market, especially in the Small-cap and Mid-cap categories, a very large AUM can become a burden. If a manager is handling ₹50,000 crores in a small-cap fund, they might find it difficult to enter and exit positions without moving the stock price. Evaluate how the manager adapts their strategy as the fund size grows.

Common Pitfalls to Avoid

- Chasing the “Star” Manager: Don’t blindly follow a manager just because they are in the news. Sometimes, the institutional process of the AMC (Asset Management Company) is more important than the individual.

- Ignoring the Team: Behind every lead manager is a team of research analysts. A strong research culture at an AMC often compensates for the departure of a lead manager.

- Short-term Panic: If a fundamentally strong manager underperforms for two quarters because their “style” (e.g., Value) is out of favor, don’t rush to redeem. Give them at least 18-24 months of underperformance before deciding to switch.

Key Takeaways

- Alpha is King: A manager’s primary job is to beat the benchmark. If they can’t do that consistently over 3-5 years, you might be better off in an index fund.

- Risk Matters: Use the Sharpe Ratio and Downside Capture Ratio to ensure the manager isn’t gambling with your money.

- Check for Style Drift: Ensure the manager is sticking to the fund’s objective and not taking unnecessary detours.

- Tenure is Crucial: Favor managers with a proven track record over multiple years and different market conditions (Bull and Bear markets).

- Skin in the Game: Check if the manager is personally invested in the fund; it ensures they are as cautious with the money as you would be.

Conclusion

Evaluating a fund manager is a mix of science and art. While metrics like CAGR, Sharpe Ratio, and Alpha provide a mathematical foundation, understanding the manager’s philosophy and tenure gives you the confidence to stay invested during volatile times. In India’s growing economy, the right fund manager can be the difference between meeting your financial goals and falling short.

Before you invest, take 15 minutes to read the Fund Manager’s profile and the fund’s latest fact sheet. It is one of the most productive things you can do for your financial future.