Equity vs Debt Funds: Which One Should You Choose?

Struggling to decide between equity and debt mutual funds? This comprehensive guide explains the differences, risks, and returns to help you build a balanced investment portfolio in India.

- NV Trends

- 6 min read

When you start your investment journey in India, the most common dilemma you will face is deciding where to put your hard-earned money. The Indian mutual fund market offers a plethora of options, but most of them fall into two primary categories: Equity Funds and Debt Funds. Choosing between them is not just about picking the one with the highest returns; it is about understanding your financial goals, your appetite for risk, and your investment horizon.

In this detailed guide, we will break down the differences between equity and debt funds to help you make an informed decision for your financial future.

What are Equity Funds?

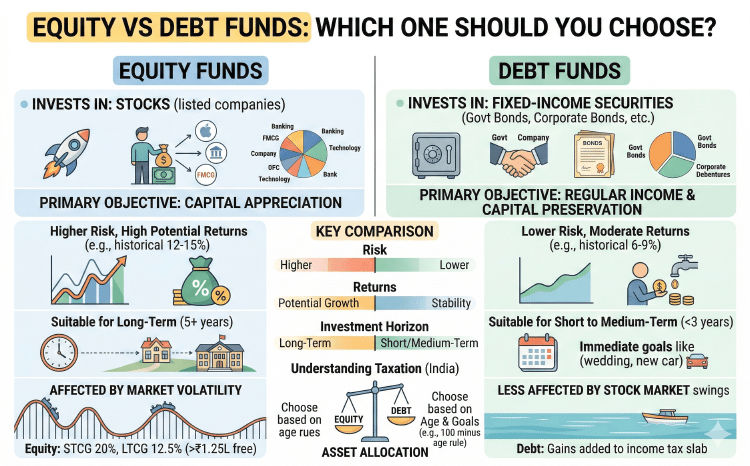

Equity funds are mutual funds that primarily invest in the stocks of listed companies. When you invest in an equity fund, you are essentially becoming a partial owner of various businesses across different sectors like Banking, Technology, Healthcare, or FMCG.

The primary objective of equity funds is capital appreciation. Since these funds track the stock market, they have the potential to deliver high returns over the long term. However, they are also subject to market volatility, meaning the value of your investment can go up or down significantly in the short term.

What are Debt Funds?

Debt funds, on the other hand, invest in fixed-income securities. These include government bonds, corporate debentures, treasury bills, and other money market instruments. When you invest in a debt fund, you are effectively lending money to the government or companies in exchange for a fixed interest rate.

The primary goal of debt funds is to provide regular income and preserve capital. They are generally considered much safer than equity funds and are less affected by stock market fluctuations. However, the returns are usually lower than what equity funds can offer over a long period.

Key Takeaways

- Equity funds invest in stocks and are suitable for long-term wealth creation (5+ years).

- Debt funds invest in fixed-income instruments and are ideal for short to medium-term goals.

- Equity carries higher risk but offers higher potential returns; Debt offers stability with moderate returns.

- A balanced portfolio usually contains a mix of both to manage risk effectively.

- Taxation rules differ significantly between equity and debt instruments in India.

Detailed Comparison: Equity vs Debt

To understand which one fits your needs, let’s compare them across several critical factors.

1. Risk Factor

Equity funds are “high risk, high reward.” Their performance depends on the business success of the companies they invest in and the overall sentiment of the stock market. If the economy is doing well, equity funds soar. If there is a recession or a market correction, they can see sharp declines.

Debt funds are “low to moderate risk.” The main risks here are interest rate changes and credit risk (the possibility that the borrower might not pay back). However, compared to the wild swings of the stock market, debt funds are very stable.

2. Potential Returns

Historically, equity funds in India have delivered returns in the range of 12% to 15% (or even higher) over a 10-year period. This makes them excellent for beating inflation.

Debt funds typically offer returns ranging from 6% to 9%, depending on the prevailing interest rates in the economy. While they might not make you “rich” overnight, they ensure your money grows steadily without keeping you awake at night during market crashes.

3. Investment Horizon

If you need money within the next 1 to 3 years—perhaps for a wedding, a down payment on a house, or an emergency fund—debt funds are your best friend. They protect your principal amount while giving better returns than a traditional savings account.

If you are planning for a goal that is 5, 10, or 20 years away—like retirement or your child’s higher education—equity funds are far superior. The power of compounding works best with equity over long durations.

Understanding the Taxation

Taxation is a crucial part of the “Equity vs Debt” debate in India, as it affects your final “in-hand” returns.

Equity Fund Taxation

- Short-term Capital Gains (STCG): If you sell your equity units within 1 year, the gains are taxed at 20%.

- Long-term Capital Gains (LTCG): If you sell after 1 year, gains up to ₹1.25 lakh in a financial year are tax-free. Gains above this limit are taxed at 12.5%.

Debt Fund Taxation

As per the latest Indian tax laws, capital gains from debt funds are added to your total income and taxed according to your applicable income tax slab rate, regardless of how long you hold them. This makes them slightly less tax-efficient for those in the 30% tax bracket compared to equity.

Which One Should You Choose?

The answer depends on who you are as an investor.

Choose Equity Funds if:

- You are young and have many years of earning ahead of you.

- You want to build a large corpus for long-term goals.

- You can stay calm even if your portfolio value drops by 10-20% in a single month.

- You want to benefit from India’s economic growth story.

Choose Debt Funds if:

- You are nearing retirement and want to protect your savings.

- You have a short-term financial goal (less than 3 years).

- You are looking for an alternative to Fixed Deposits (FDs).

- You have a very low tolerance for risk and prefer peace of mind over high returns.

The Secret: Asset Allocation

You don’t actually have to choose just one! The most successful Indian investors use a strategy called “Asset Allocation.” This means you divide your money between equity and debt based on your age and goals.

A common rule of thumb is “100 minus your age.” If you are 30 years old, you could keep 70% in equity and 30% in debt. As you get older, say 50, you shift to 50% equity and 50% debt to reduce risk. This balanced approach allows you to enjoy the growth of the stock market while having the safety net of bond investments.

Conclusion

Both equity and debt funds play vital roles in a healthy financial plan. Equity is the “accelerator” that helps your wealth grow fast, while debt is the “brake” that provides stability during bumpy rides. Instead of trying to find the “perfect” fund, focus on your goals. Use debt funds for your immediate needs and equity funds for your future dreams.

Before making any large investment, it is always wise to consult with a certified financial planner who can tailor a portfolio specifically for your family’s needs.