Understanding Capital Gains Tax in India

A comprehensive guide to understanding Short-Term and Long-Term Capital Gains tax in India, covering equity, debt, real estate, and gold for the financial year 2025-26.

- NV Trends

- 6 min read

For any Indian investor, the excitement of watching an investment grow is often tempered by a single, unavoidable question: “How much tax will I have to pay on this profit?” Whether you are trading stocks on the NSE, investing in mutual funds through an SIP, or selling a family property, understanding Capital Gains Tax is crucial to knowing your actual “in-hand” returns.

In India, the tax laws surrounding capital gains have undergone significant changes in recent years, particularly with the Union Budget updates. As we navigate 2026, it is more important than ever to stay updated on how the government views your profits. This guide will break down the complexities of capital gains into simple, easy-to-understand sections.

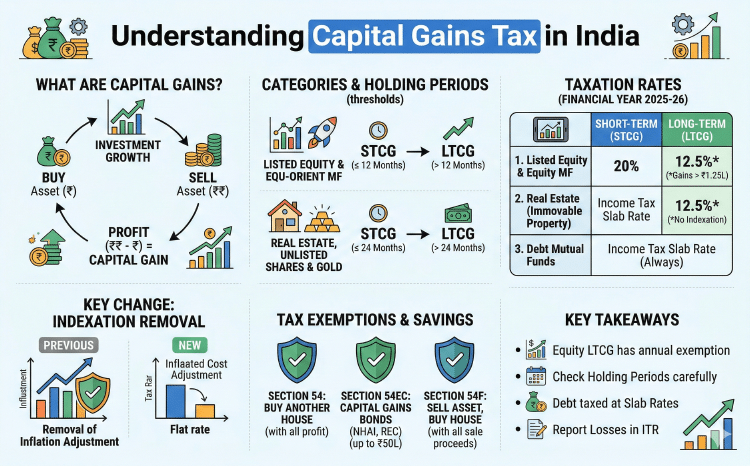

What Exactly are Capital Gains?

A “Capital Gain” is simply the profit you make when you sell a “Capital Asset” for more than what you paid for it. A capital asset includes almost everything you own for investment or personal use—stocks, bonds, mutual fund units, real estate, gold, and even certain types of jewelry.

However, the Income Tax Department doesn’t treat all profits equally. The tax you pay depends on two main factors:

- The type of asset you sold.

- How long you held the asset before selling it (the “Holding Period”).

This brings us to the two broad categories of capital gains: Short-Term Capital Gains (STCG) and Long-Term Capital Gains (LTCG).

Holding Periods: The Divider Between STCG and LTCG

The holding period is the duration for which you owned the asset. Depending on this duration, your gain is classified as either short-term or long-term. Following the recent streamlining of tax laws, the holding periods are generally categorized as follows:

Listed Equity and Equity-Oriented Mutual Funds

For stocks listed on Indian exchanges and mutual funds that invest more than 65% in Indian equities, the threshold is 12 months.

- STCG: If sold within 1 year.

- LTCG: If sold after 1 year.

Real Estate and Unlisted Shares

For immovable property (land or house) and shares of companies not listed on a stock exchange, the threshold is 24 months.

- STCG: If sold within 2 years.

- LTCG: If sold after 2 years.

Other Assets (Gold and Debt Instruments)

For physical gold, gold ETFs, and most other assets, the holding period for long-term classification used to be 36 months, but recent rules have moved many of these toward a 24-month or 12-month standard depending on the specific instrument. It is important to note that since April 2023, debt mutual funds no longer enjoy LTCG benefits and are taxed at your income tax slab rate regardless of the holding period.

Taxation Rates for 2025-2026

The tax rates were recently revised to simplify the structure. Here is how your profits are taxed in the current financial environment:

1. Listed Equity and Equity Mutual Funds

Equity remains one of the most tax-efficient ways to grow wealth in India, despite the rates moving up slightly.

- Short-Term Capital Gains (STCG): These are taxed at a flat rate of 20%.

- Long-Term Capital Gains (LTCG): These are taxed at 12.5%. However, there is a significant relief: gains up to ₹1.25 Lakh in a financial year are completely exempt from tax. You only pay 12.5% on the amount exceeding this limit.

2. Real Estate (Immovable Property)

The taxation of property has seen a major shift.

- Short-Term Capital Gains (STCG): The profit is added to your total income and taxed according to your applicable income tax slab rate (10%, 20%, or 30%).

- Long-Term Capital Gains (LTCG): These are now taxed at a flat rate of 12.5% without the benefit of indexation for properties acquired after the recent rule changes. For older properties, there are specific grandfathering clauses that allow taxpayers to choose between different regimes.

3. Debt Mutual Funds

Debt funds are now treated differently to bring them on par with Fixed Deposits (FDs).

- Taxation: All gains from debt mutual funds (where equity exposure is less than 35%) are treated as short-term and taxed at your income tax slab rate. There is no longer a “Long-Term” benefit for new investments in this category.

4. Gold and Silver

- STCG: Added to income and taxed at slab rates.

- LTCG: Taxed at 12.5%.

The Disappearance of Indexation

One of the biggest changes in the Indian tax landscape recently has been the removal of “Indexation” for most asset classes. Indexation allowed investors to adjust the purchase price of an asset against inflation using the Cost Inflation Index (CII). This effectively reduced the “taxable profit.”

While the removal of indexation sounds negative, the government compensated by lowering the LTCG tax rate from 20% to 12.5%. For most investors holding assets for a moderate period, the lower flat rate is intended to simplify calculations and reduce the tax burden, though real estate investors in slow-growing areas might find it less beneficial.

How to Save Capital Gains Tax: Exemptions

The Indian Income Tax Act offers several ways to legally reduce or eliminate your capital gains tax liability, especially when selling property.

Section 54: Investing in another House

If you sell a residential house and make a long-term capital gain, you can avoid paying tax by using the entire profit to buy another residential house in India. You must buy the new house either one year before or two years after the sale of the old one.

Section 54EC: Capital Gains Bonds

If you don’t want to buy another house, you can invest your LTCG (up to ₹50 Lakh) in specific government-notified bonds like those issued by NHAI (National Highways Authority of India) or REC (Rural Electrification Corporation). These bonds have a lock-in period of 5 years.

Section 54F: Selling Assets other than a House

If you sell gold or shares and have a large long-term capital gain, you can claim an exemption by investing the entire sale proceeds (not just the profit) into a residential house property.

Setting Off and Carrying Forward Losses

Not every investment results in a profit. If you have made a loss, you can use it to your advantage:

- Short-Term Capital Loss (STCL): Can be set off against both Short-Term and Long-Term Capital Gains.

- Long-Term Capital Loss (LTCL): Can only be set off against Long-Term Capital Gains.

If you cannot set off the entire loss in a single year, you can “carry forward” the loss for up to 8 assessment years, provided you file your income tax return (ITR) on time.

Key Takeaways

- Equity Advantage: Equity LTCG is taxed at 12.5% with a ₹1.25 Lakh annual exemption, making it great for long-term wealth.

- Holding Period Matters: Ensure you know if your asset needs 12 or 24 months to qualify for the lower LTCG rates.

- Debt is Slab-Based: Mutual funds with low equity exposure are now taxed like interest income.

- Report Losses: Always file your ITR to carry forward losses; they are valuable tools to reduce future tax bills.

- Plan Property Sales: Use Section 54 or 54EC if you are selling a house to save significantly on taxes.

Conclusion

Taxation is an integral part of the investment cycle. While the primary goal of investing is to generate returns, a smart investor always keeps an eye on the “net return” after taxes. The shift towards a flat 12.5% LTCG rate and the removal of indexation marks a move toward a simpler tax regime in India.

By aligning your investment horizon with the required holding periods and utilizing available exemptions like Section 54, you can ensure that you keep a larger portion of your hard-earned profits. Always consult with a tax professional for specific transactions, as rules can vary based on individual circumstances and the timing of the sale.