Best Tax-Free Bonds for 2026

Discover the best tax-free bonds in India for 2026. Learn how to earn steady, tax-exempt income while preserving your capital with low-risk government-backed investments.

- NV Trends

- 5 min read

In the Indian investment landscape, the search for “safe” returns often leads people to Fixed Deposits (FDs). However, as tax brackets rise and inflation eats into real returns, smart investors are looking for alternatives that offer a rare benefit: 100% tax-free income. Tax-free bonds have emerged as a premier choice for those in the 30% tax bracket who want to keep every rupee they earn.

As we move through 2026, the interest rate cycle and the government’s infrastructure push have made certain tax-free bonds particularly attractive. This guide will help you understand how these bonds work and which ones are the best options for your portfolio this year.

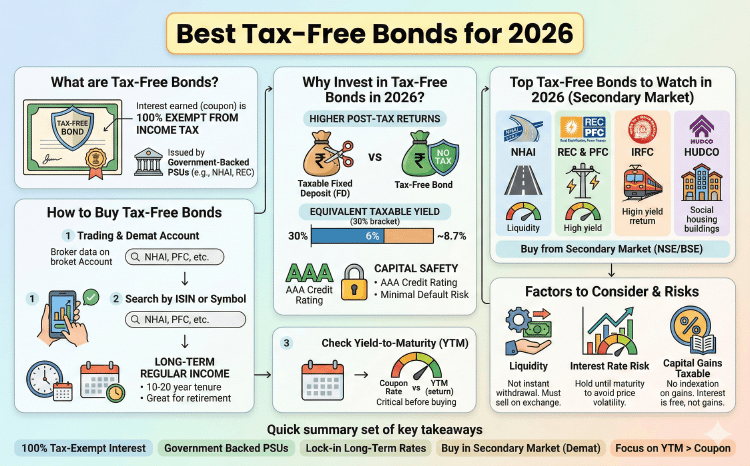

What are Tax-Free Bonds?

Tax-free bonds are fixed-income instruments issued by government-backed entities. These are typically public sector undertakings (PSUs) involved in infrastructure, housing, and power. The primary lure of these bonds is that the interest earned (coupon) is completely exempt from income tax under Section 10(15)(iv)(h) of the Income Tax Act.

Unlike a Fixed Deposit, where the bank deducts TDS and you pay tax according to your slab, the annual interest from these bonds arrives in your bank account without any deductions.

Why Should You Invest in Tax-Free Bonds in 2026?

The financial environment in 2026 has made these instruments highly relevant for several reasons:

1. High Post-Tax Returns

For an investor in the 30% tax bracket, a tax-free bond offering 6% is equivalent to a taxable FD offering nearly 8.7%. Finding an FD with that rate from a AAA-rated bank is increasingly difficult, making bonds a superior choice for high-net-worth individuals.

2. Capital Safety

Most tax-free bonds are issued by entities like NHAI (National Highways Authority of India), REC (Rural Electrification Corporation), and PFC (Power Finance Corporation). These carry the highest credit ratings (AAA), offering a level of security that is second only to direct government debt.

3. Long-Term Regular Income

These bonds usually have long tenures, often ranging from 10 to 20 years. This allows you to lock in a fixed rate of interest for a long duration, which is perfect for retirement planning or creating a steady secondary income stream.

Best Tax-Free Bonds to Watch in 2026

While the primary market (new issues) for tax-free bonds has been quiet, the secondary market on the NSE and BSE is thriving. Here are the top picks based on liquidity and yield-to-maturity (YTM):

NHAI Tax-Free Bonds

The National Highways Authority of India remains the gold standard. Their bonds are highly liquid, meaning you can buy or sell them relatively easily on the stock exchange. They are backed by the central government’s infrastructure initiatives, making them incredibly safe.

REC and PFC Bonds

Rural Electrification Corporation and Power Finance Corporation are the backbones of India’s power sector. Their bonds often offer slightly higher yields than NHAI while maintaining a stellar credit profile. In 2026, with the focus on renewable energy, these entities are financially robust.

IRFC (Indian Railway Finance Corporation)

If you want to bet on the growth of Indian Railways, IRFC bonds are an excellent pick. They generally offer consistent coupon payments and have a very low risk of default given their strategic importance to the country.

HUDCO (Housing and Urban Development Corporation)

HUDCO bonds are another great option, particularly for those looking for diversification. They focus on social infrastructure and housing, often providing competitive yields in the secondary market.

How to Buy Tax-Free Bonds

Since the government hasn’t issued fresh tax-free bonds in recent years, you must buy them through the secondary market.

- Trading Account: You need a standard Demat and trading account.

- Search by ISIN or Symbol: You can search for these bonds on your broker’s app using names like “NHAI,” “RECLTD,” or “PFC.”

- Check Yield to Maturity (YTM): Don’t just look at the coupon rate. Look at the YTM, which tells you the actual return you will get if you buy the bond at the current market price and hold it until maturity.

Factors to Consider Before Investing

While the tax benefits are great, you should be aware of a few nuances:

Interest Rate Risk

If market interest rates rise significantly, the price of your bond in the secondary market might fall. This only matters if you intend to sell before maturity. If you hold until the end, you get your principal back in full.

Liquidity

Unlike a savings account, you cannot always “withdraw” your money instantly. You have to sell the bond on the exchange. For large volumes, it might take a few days to find a buyer at your desired price.

No Tax Benefit on Capital Gains

While the interest is tax-free, any capital gains (profit made if you sell the bond at a higher price than you bought it) are taxable. Long-term capital gains on listed bonds are generally taxed at 10% without indexation.

Who Should Invest?

Tax-free bonds are not for everyone. They are most suitable for:

- Investors in the 20% or 30% tax brackets.

- Retirees looking for monthly or annual income without tax headaches.

- Conservative investors who prioritize capital preservation over high-risk growth.

- Individuals looking to diversify away from pure equity or gold.

Key Takeaways

- Tax Efficiency: Every rupee earned as interest is 100% tax-exempt in the hands of the investor.

- Government Backing: High credit safety as most issuers are government-owned PSUs like NHAI, REC, and IRFC.

- Lock-in Advantage: Great for long-term goals, allowing you to lock in interest rates for 10-15 years.

- Secondary Market Entry: Since new issues are rare, investors must use a Demat account to buy existing bonds from the stock exchange.

- YTM is Critical: Always calculate the Yield to Maturity before buying to understand the real return on your investment.

Conclusion

Tax-free bonds remain one of the most effective tools for tax planning in India. In 2026, as the market stabilizes, these instruments provide a unique combination of safety and tax-free income that taxable instruments simply cannot match. By focusing on high-liquidity bonds like those from NHAI and REC, you can build a stable foundation for your fixed-income portfolio.

Before investing, ensure that the maturity date aligns with your financial goals and that you are comfortable with the long-term nature of these assets. For those in high tax brackets, these are perhaps the “best-kept secrets” for generating wealth without sharing a large portion with the tax department.