How to Avoid Common Investment Mistakes

Learn how to identify and avoid the most common investment mistakes that Indian investors make, from panic selling to lack of diversification.

- NV Trends

- 6 min read

Investing is often seen as a complex game of numbers, charts, and market predictions. However, for most successful investors in India, it is less about making brilliant moves and more about avoiding basic errors. As the saying goes, “Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.”

In the Indian context, where the market is vibrant and full of opportunities, it is easy to get carried away by emotions, neighborhood tips, or the fear of missing out (FOMO). Whether you are investing in mutual funds, direct stocks, or gold, avoiding common pitfalls can significantly enhance your long-term wealth.

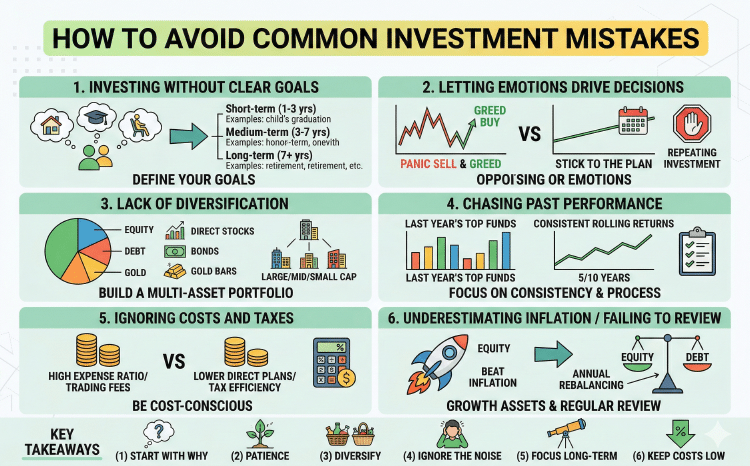

1. Investing Without a Clear Goal

One of the biggest mistakes Indian investors make is “investing for the sake of investing.” You might start a Systematic Investment Plan (SIP) because a friend did, or buy a tax-saving instrument at the last minute in March.

Without a goal, you won’t know how much to invest, where to invest, or for how long. Are you saving for your child’s higher education? Your retirement? Or a down payment for a house? Each goal has a different time horizon and requires a different asset allocation.

The Fix: Goal-Based Investing

Before putting a single rupee into the market, define your goals. Categorize them into short-term (1-3 years), medium-term (3-7 years), and long-term (7+ years). This clarity will help you choose between debt funds, balanced funds, or aggressive equity funds.

2. Letting Emotions Drive Decisions

The stock market is a rollercoaster. When the Sensex is at an all-time high, everyone wants to invest. When it crashes, everyone wants to pull their money out. This “buy high, sell low” behavior is the exact opposite of what a successful investor should do.

Fear and greed are the two biggest enemies of your portfolio. Panic selling during a market correction is the surest way to turn a temporary notional loss into a permanent real loss.

The Fix: Stick to the Plan

Automate your investments through SIPs. This removes the emotional element of trying to “time” the market. Remember that market volatility is a feature, not a bug. If your fundamental reason for investing hasn’t changed, don’t let a temporary dip scare you away.

3. Lack of Diversification (Putting All Eggs in One Basket)

We often see investors who are overly concentrated in one area. Some might have 90% of their wealth in physical real estate, while others might only invest in a single sector like Information Technology (IT) because it performed well in the past.

If that specific sector or asset class faces a downturn, your entire portfolio suffers. Diversification is your only “free lunch” in finance.

The Fix: Build a Multi-Asset Portfolio

A healthy portfolio should be spread across different asset classes like equity, debt, and gold. Within equity, you should diversify across large-cap, mid-cap, and small-cap stocks. Mutual funds are an excellent way for retail investors to achieve this diversification instantly.

4. Chasing Past Performance

Many investors look at the “Top Funds of Last Year” list and invest their money there. However, the best-performing fund of last year is rarely the best-performing fund of the next year. Often, a fund tops the charts because a specific sector or style was in favor, which might mean it is now overvalued.

The Fix: Focus on Consistency and Process

Instead of looking at a single year’s return, look at the fund’s performance over 5-year or 10-year periods. More importantly, look at the “rolling returns” to see how the fund performed during market cycles. Check the fund manager’s track record and the investment philosophy of the fund house.

5. Ignoring the Impact of Costs and Taxes

While a 1% expense ratio or a 10% capital gains tax might seem small, they have a massive impact over 20 years due to the loss of compounding. Many investors fail to account for the “leakage” in their returns caused by high-commission regular plans or frequent trading that triggers short-term capital gains tax.

The Fix: Be Cost-Conscious

Consider investing in Direct Plans of mutual funds if you are comfortable doing your own research; they have lower expense ratios than Regular Plans. Also, be aware of the tax rules: equity investments held for more than a year are taxed as Long-Term Capital Gains (LTCG) at 12.5% (above a ₹1.25 lakh limit), which is much lower than short-term rates.

6. Underestimating Inflation

Many Indian families still rely heavily on traditional savings like Fixed Deposits (FDs) or Savings Accounts. While these are safe, they often fail to beat inflation. If inflation is 6% and your FD gives 7% before tax, your real return after tax is almost zero or even negative.

The Fix: Asset Allocation for Growth

To build wealth, you need assets that grow faster than the cost of living. Equity is one of the few asset classes that has historically beaten inflation over the long term. Ensure a portion of your portfolio is dedicated to growth assets.

7. Failing to Review the Portfolio

Investing isn’t a “set it and forget it” task. Over time, your asset allocation can shift. For example, if the stock market has a great run, your portfolio might become 80% equity when you originally intended it to be 60%. This increases your risk without you realizing it.

The Fix: Annual Rebalancing

Review your portfolio at least once a year. If your equity portion has grown too large, sell some and move it to debt to bring it back to your target ratio. This forces you to “sell high” and “buy low” systematically.

Key Takeaways

- Start with a Why: Always link your investments to specific financial goals.

- Patience is a Virtue: The real magic happens in the 10th, 15th, and 20th years of compounding.

- Diversify: Spread your risk across sectors and asset classes to protect your downside.

- Ignore the Noise: Don’t follow “hot tips” from social media or news channels.

- Focus on the Long Term: Short-term market movements are unpredictable; long-term trends are much more reliable.

- Keep Costs Low: Small savings in fees and taxes result in lakhs of extra rupees over time.

Conclusion

Avoiding investment mistakes is often about discipline and temperament rather than intelligence. The most successful investors in India are not necessarily those who found the “next multibagger” stock, but those who stayed invested through the ups and downs and didn’t make the mistakes mentioned above.

By defining your goals, diversifying your assets, and keeping your emotions in check, you can navigate the Indian markets with confidence. Remember, the goal of investing is to provide for your future self, and the best way to do that is to stay the course and keep it simple.